Will the UK Wealth Management M&A Boom Continue in 2026 and Beyond? A Reality Check

The Market Is Not Slowing Down. It Is Getting Ruthlessly Selective.

For the last several years, UK wealth management has been one of the most attractive consolidation stories in European financial services.

Private equity firms entered the market aggressively. Consolidators scaled rapidly. Valuations increased materially. Every conference panel, every industry report, and virtually every sell-side process repeated the same narrative:

fragmentation + recurring revenues + demographics = unstoppable consolidation.

For a while, that narrative was broadly correct.

The problem is that many market participants still think they are operating in that market.

They are not.

The UK wealth management M&A market has not stopped growing. Capital has not disappeared. Private equity interest has not collapsed. In fact, many of the long-term structural drivers behind consolidation are arguably stronger today than they were five years ago, which is why we actually seeing growing private equity interest in UK wealth management.

But the market has fundamentally changed in one critical respect:

buyers no longer reward businesses equally.

That distinction is becoming the defining feature of UK wealth management M&A in 2026.

The market did not slow down.

It split - a fact that is underestimated by many.

And increasingly, the firms achieving exceptional outcomes are not necessarily the largest firms. They are the firms buyers believe will matter inside the next ownership cycle.

That is a very different market from the one that existed during the earlier expansion phase.

The Most Dangerous Misunderstanding in the Market

One of the biggest mistakes founders, management teams, and even some investors continue to make is assuming that the current market is simply a continuation of the 2019–2023 consolidation cycle.

It is not.

During the earlier phase of consolidation:

capital availability was extremely abundant;

scalable assets were relatively scarce;

and many buyers were still trying to establish positions within the sector.

As a result, a large proportion of the market benefited from broad valuation expansion.

In practical terms, many firms achieved strong outcomes simply because they operated within an attractive sector.

That environment is evolving rapidly.

According to Dyer Baade & Company proprietary market research, the UK wealth management market is now transitioning from: an expansion market to a selection market.

That distinction matters enormously.

Earlier in the cycle, buyers competed aggressively simply to gain exposure to the sector.

Today, buyers increasingly compare:

multiple platform assets,

multiple bolt-on opportunities,

and multiple strategic alternatives simultaneously.

This naturally changes buyer behaviour.

The market is becoming:

more selective,

more institutional,

more diligence-heavy,

and significantly more strategic.

That is why some firms continue achieving exceptional valuations while others increasingly struggle to create genuine competitive tension.

The Structural Drivers Behind the Boom Are Still Extremely Strong

Ironically, many of the people predicting a slowdown focus heavily on short-term transaction sentiment while ignoring the fact that the long-term structural investment thesis behind UK wealth management remains exceptionally powerful.

Almost none of the major drivers behind consolidation have disappeared.

If anything, several have strengthened.

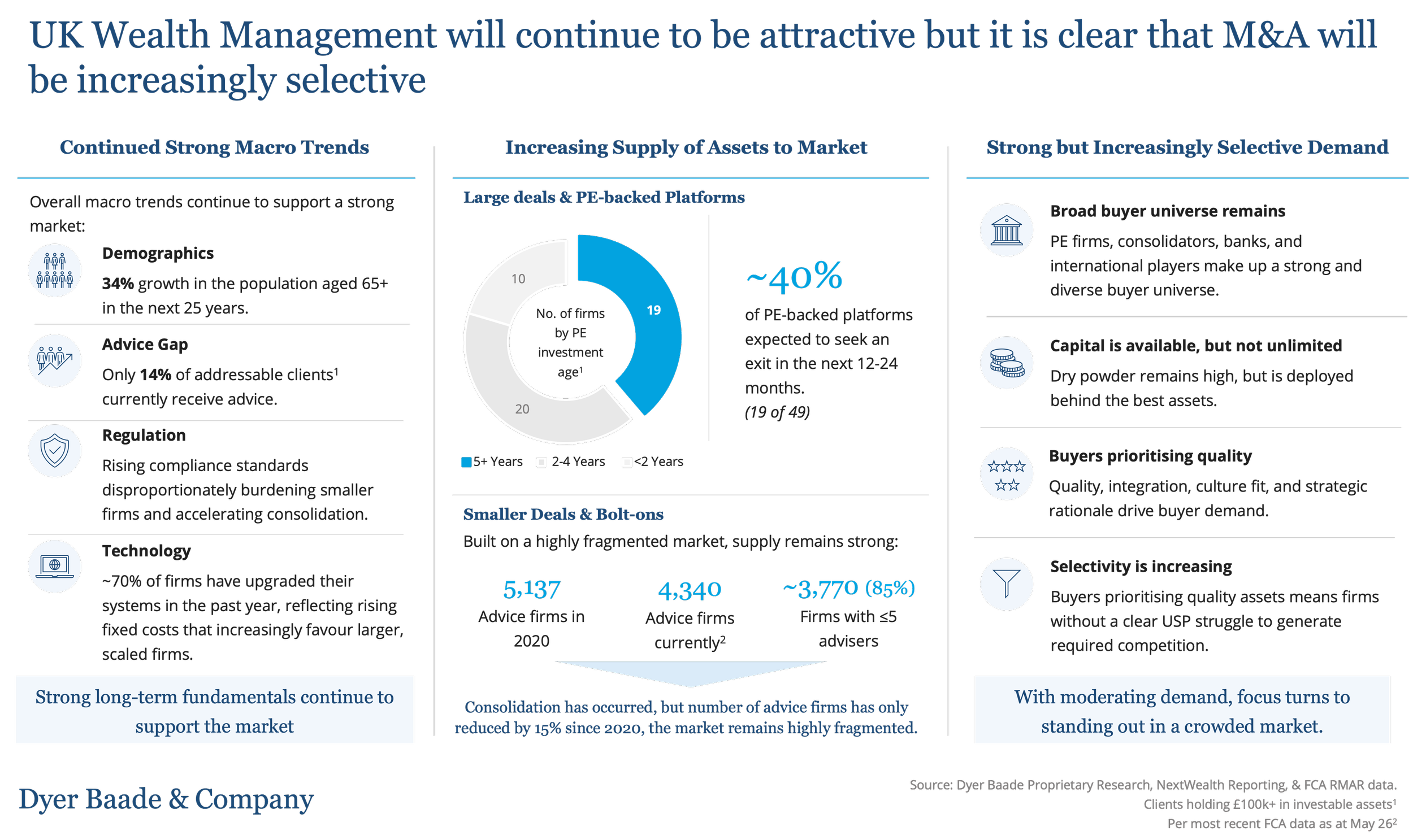

Demographics Are Still Creating a Massive Long-Term Tailwind

One of the most underappreciated realities in UK financial services is that wealth management remains fundamentally tied to demographic rather than cyclical trends.

The UK population aged 65 and over is expected to grow by approximately 34% over the next 25 years.

That matters enormously.

Why?

Because ageing populations directly increase demand for:

retirement planning,

wealth preservation,

inheritance structuring,

intergenerational wealth transfer,

and ongoing investment advice.

Unlike many sectors, wealth management benefits from long-duration demographic expansion rather than short-term consumer demand cycles.

Sophisticated investors understand this clearly.

This is one reason private equity firms continue viewing wealth management as one of the most structurally attractive consolidation opportunities in UK financial services.

The Advice Gap Is Still Enormous

The advice gap remains one of the strongest long-term growth drivers in the market.

Despite the size of the UK wealth pool, only approximately 14% of addressable consumers currently receive regulated financial advice.

That statistic is extraordinary.

It means the overwhelming majority of consumers with meaningful investable assets still operate without professional wealth management support.

From a strategic perspective, this creates two simultaneous opportunities:

organic growth potential;

consolidation potential.

The market is not saturated.

In many respects, it remains significantly underpenetrated.

This is one reason private equity firms continue deploying capital aggressively into the sector despite increasing market maturity.

Fragmentation Still Makes Consolidation Almost Inevitable

The fragmentation story also remains intact.

Despite years of consolidation activity, the UK wealth management and IFA market remains highly fragmented relative to many other financial services sectors.

According to industry data referenced in Dyer Baade & Company proprietary research, more than 85% of advisory firms still operate with five advisers or fewer.

That is a remarkably fragmented market structure.

And fragmentation matters because fragmentation creates:

acquisition opportunity,

operational inefficiency,

and scalability arbitrage.

In practical terms, the addressable acquisition universe remains enormous.

This is one reason the long-term M&A thesis remains fundamentally attractive even as the market itself becomes more selective.

Regulation Is Quietly Accelerating Consolidation

One of the least appreciated drivers of consolidation is regulation itself.

Increasing FCA expectations around:

compliance,

operational resilience,

consumer duty,

reporting,

and technology infrastructure

are materially increasing operational complexity across the sector.

Large firms absorb these costs relatively efficiently.

Small firms increasingly struggle.

This creates a structural economic pressure toward scale.

The consequence is straightforward:

many smaller firms increasingly face three realistic options:

invest heavily,

partner strategically,

or sell.

This is one reason the long-term supply of acquisition opportunities is unlikely to disappear any time soon.

Technology Is Creating a Two-Speed Industry

Technology is accelerating the same trend.

Modern wealth management increasingly requires:

integrated CRM infrastructure,

workflow automation,

scalable reporting systems,

compliance technology,

and sophisticated client engagement capabilities.

These investments require:

capital,

operational sophistication,

and scale.

Larger consolidators increasingly benefit from operational leverage.

Smaller firms increasingly fall behind.

The result is a two-speed market:

firms becoming increasingly institutionalised;

and firms gradually becoming operationally obsolete.

That divergence is becoming one of the defining characteristics of the sector.

Private Equity Interest Has Not Weakened - Competition Has Intensified

One of the most misunderstood developments in the market is the assumption that private equity appetite has weakened.

It has not.

If anything, competition among buyers has intensified.

According to Dyer Baade & Company proprietary market analysis, the number of PE-backed consolidators continues increasing even as overall bolt-on transaction volumes have stabilised.

That dynamic matters enormously.

It means:

more capital is now competing for a relatively stable pool of attractive acquisition opportunities.

This naturally creates two consequences:

stronger competition for premium assets;

greater selectivity around average assets.

That is precisely what is happening today.

So Why Are Some People Talking About a Slowdown?

One of the most interesting dynamics in the current market is the growing disconnect between public market optimism and what many industry insiders are quietly discussing behind closed doors.

Publicly, the narrative around UK wealth management M&A often remains overwhelmingly positive:

strong demographics,

recurring revenues,

fragmented markets,

and continued private equity interest.

All of those points remain broadly correct.

However, beneath the surface, the market has become materially more difficult to navigate than it was several years ago.

Industry participants increasingly recognise several emerging realities:

a number of PE-backed consolidators have quietly explored exit options without ultimately completing transactions;

transactions that do complete are often taking significantly longer;

and deal structures are becoming materially more complex.

These developments are important because they signal a market that is maturing.

Earlier in the consolidation cycle, many PE-backed platforms benefited from exceptionally strong momentum. Capital was abundant, scaled assets were relatively scarce, and buyers were often competing aggressively simply to gain exposure to the sector.

Today, that dynamic is evolving.

As more PE-backed consolidators approach the stage where they would typically seek liquidity events, buyers are increasingly able to compare multiple scaled assets simultaneously. In practical terms, this creates more competition not just among buyers - but increasingly among sellers as well.

This naturally increases selectivity.

Importantly, this does not mean that transactions are no longer happening. Far from it. High-quality businesses continue to attract very strong interest and premium valuations.

However, the environment has become materially more sophisticated and materially less forgiving and most founder-led firms are structurally unprepared for what that means.

Many industry participants privately acknowledge that processes which would likely have cleared relatively quickly in 2021–2022 now face materially deeper scrutiny.

In some very recent cases, businesses have tested buyer appetite only to discover that valuation expectations, integration concerns, financing structures, or future exit questions create more friction than anticipated.

Equally important, deal structures themselves are becoming more nuanced.

Historically, many transactions were relatively simple control deals driven by broad market momentum. Today, transactions increasingly involve:

deferred consideration,

rollover structures,

minority reinvestment dynamics,

platform integration considerations,

management incentive redesign,

and more sophisticated alignment structures between buyers and sellers.

This is particularly true in larger platform and secondary PE transactions where buyers are underwriting not only current earnings, but also future scalability and future exit optionality.

As the market matures, complexity is increasing.

That trend is likely to continue over the coming years as:

more PE-backed consolidators approach exit simultaneously;

buyers become more selective;

and operational quality becomes increasingly important relative to simple scale.

This has major implications for privately owned wealth management firms considering strategic options.

Five years ago, many businesses could achieve strong outcomes primarily because the sector itself was highly attractive. Today, premium outcomes increasingly require:

sharper positioning,

stronger preparation,

more targeted buyer selection,

and significantly more sophisticated process management.

In other words:

the quality of the process increasingly matters almost as much as the quality of the asset itself.

This is one reason specialist sector expertise is becoming substantially more valuable in wealth management M&A.

As buyers become more institutional and transactions become more complex, advisers increasingly need:

deep sector-specific understanding,

credibility with sophisticated buyers,

direct knowledge of platform dynamics,

and real experience navigating complex PE-backed processes.

As transactions become more institutional and strategically complex, sector-specific execution capability increasingly influences not only valuation outcomes, but whether transactions complete successfully at all.

Having advised on more than 40 wealth management transactions across the UK market, Dyer Baade & Company has seen first-hand how materially outcomes can diverge depending on:

positioning,

process structure,

buyer strategy,

and transaction execution.

In a market that is becoming progressively more selective and strategically driven, these factors increasingly influence not only valuation - but whether a transaction successfully completes at all.

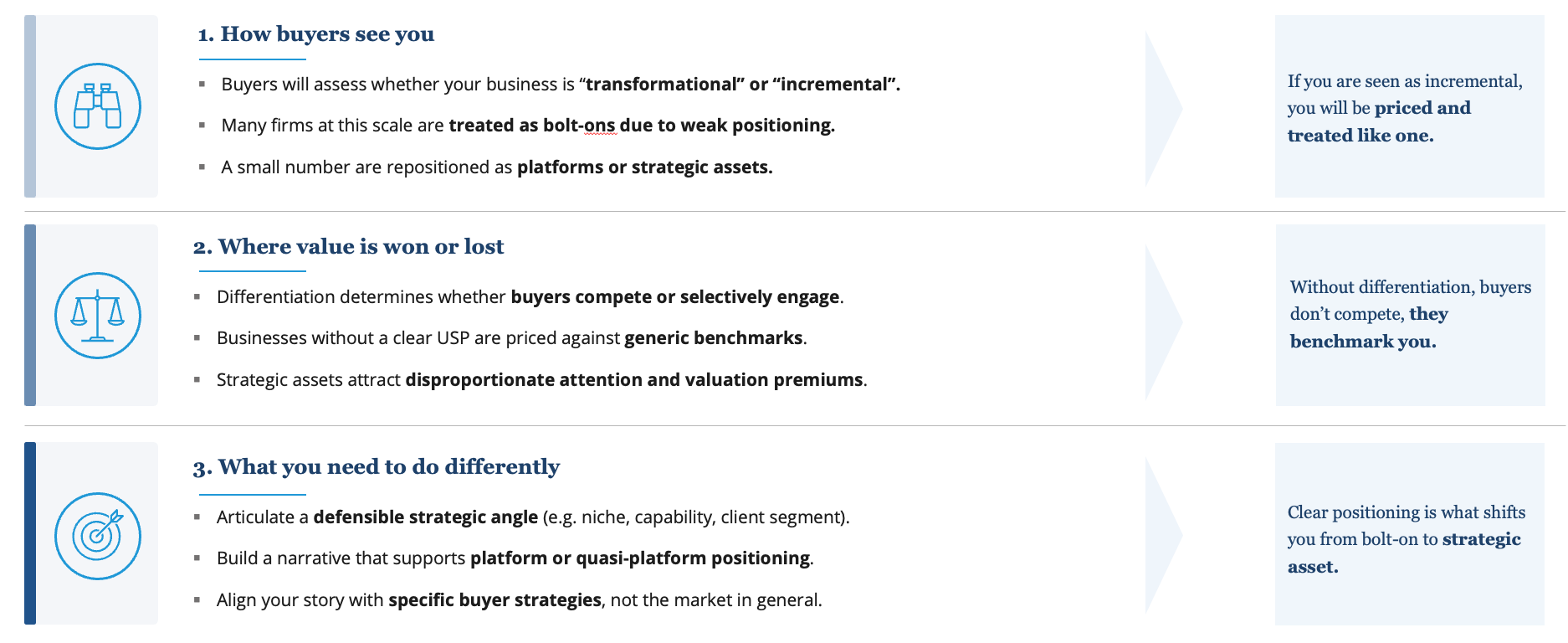

The Market Is No Longer Paying Premium Valuations for Participation

This is the single most important shift currently occurring in UK wealth management M&A.

Earlier in the cycle, broad market momentum often lifted almost all businesses.

Today, buyers increasingly differentiate aggressively between:

strategic assets;

and replaceable businesses.

This distinction is becoming brutal.

Sophisticated buyers increasingly ask:

does this acquisition improve platform quality?

does it strengthen future exit optionality?

does it scale operationally?

does it improve strategic positioning?

would future buyers pay a premium for this asset?

Those are fundamentally different questions from: “Is this a good business?”

And that change explains why valuation dispersion is widening so dramatically.

In practice, this means businesses that would have achieved premium outcomes three years ago may now struggle to generate genuine buyer competition.

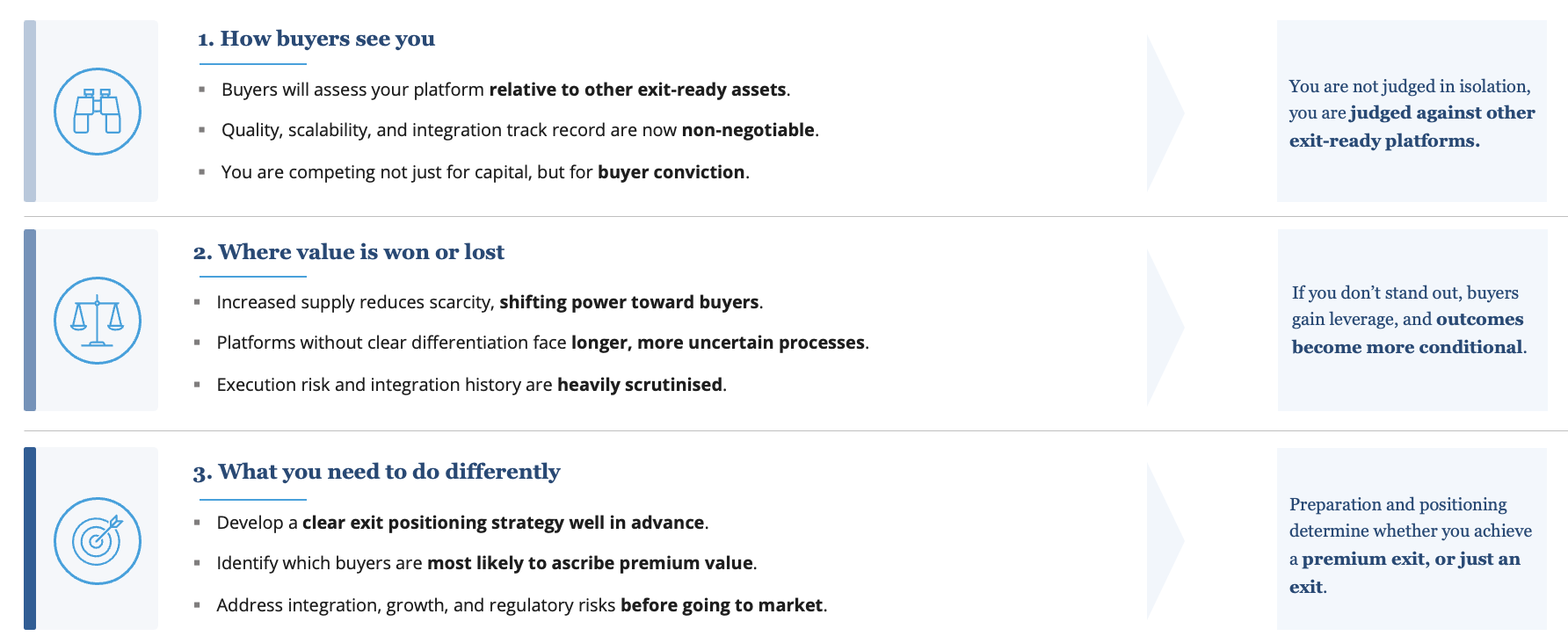

The Market Is Entering the PE Exit Era

One of the most important structural developments over the next several years will be the increasing number of PE-backed platforms approaching exit.

Historically, relatively few scaled wealth management platforms came to market in any given year.

That is changing.

As more PE-backed consolidators mature simultaneously, buyers will increasingly compare:

multiple platform exits,

multiple secondary opportunities,

and multiple strategic alternatives.

This naturally creates:

more buyer discipline,

deeper diligence,

greater scrutiny around scalability,

and greater focus on operational quality.

In practical terms:

the market is becoming institutional.

That changes valuation dynamics materially.

Buyers Are Becoming Much More Sophisticated

Earlier phases of consolidation often rewarded acquisition activity itself.

Growth narratives alone could support premium valuations.

Today, sophisticated buyers increasingly care about:

integration quality,

operational robustness,

client retention,

infrastructure scalability,

and management depth.

The market is no longer rewarding growth at any cost.

It is rewarding:

scalable, defensible, institutional growth.

That distinction matters enormously for PE-backed platforms approaching exit.

Future buyers increasingly want evidence that prior acquisitions genuinely created value rather than simply increased scale superficially.

The Era of Generic M&A Processes Is Ending

Another major shift is process sophistication. The days of broad auction processes automatically generating strong outcomes are disappearing. Today, buyers are overwhelmed with opportunities.

Generic positioning increasingly creates generic outcomes. Premium valuation outcomes increasingly depend on:

strategic positioning,

buyer targeting,

narrative control,

and process sophistication.

This is one reason adviser selection is becoming much more important.

In an increasingly selective market, sector-specific expertise can materially influence:

buyer perception,

competitive tension,

strategic positioning,

and ultimately valuation outcomes.

Generalist advisers often still run wealth management transactions as traditional mid-market M&A processes.

Sophisticated buyers no longer engage with the sector that way.

Having advised on more than 40 wealth management transactions across the UK market, Dyer Baade & Company has seen first-hand how businesses with similar underlying financial profiles can achieve dramatically different outcomes depending on:

positioning,

buyer selection,

strategic narrative,

and process execution.

In many respects, premium outcomes are increasingly engineered long before buyers formally enter the process.

For founders and management teams, the key question is no longer whether capital exists in the sector.

For founders and management teams, the key question is no longer whether capital exists in the sector. The key question is whether buyers will view the business as strategically essential - or operationally replaceable.

That distinction increasingly determines valuation outcomes.

What This Means for Sellers

For founders and shareholders considering a sale, the current market remains highly attractive - but it also requires greater sophistication than before. The positive news is that:

buyer demand remains broad,

capital availability remains strong,

and long-term sector fundamentals continue to support M&A activity.

However, sellers should not assume that market conditions alone will produce premium outcomes. Increasingly, valuation depends on:

how a business is positioned,

how scalable it is,

how strategically relevant it appears,

and how effectively it is prepared for diligence.

This is particularly relevant for medium-sized firms and larger bolt-ons, where buyers are increasingly differentiating between:

strategic assets,

and incremental acquisitions.

What This Means for PE-Backed Platforms

For PE-backed consolidators approaching exit, the market is becoming more competitive. Buyers are comparing assets more directly than in earlier phases of the cycle. This is where the market is quietly changing. As a result, businesses increasingly need to demonstrate:

operational maturity,

scalable infrastructure,

integration capability,

and a credible long-term growth story.

The market is no longer rewarding growth alone. It is rewarding growth that appears scalable, sustainable, and institutionally robust. This means that preparation and positioning are becoming increasingly important determinants of exit outcomes.

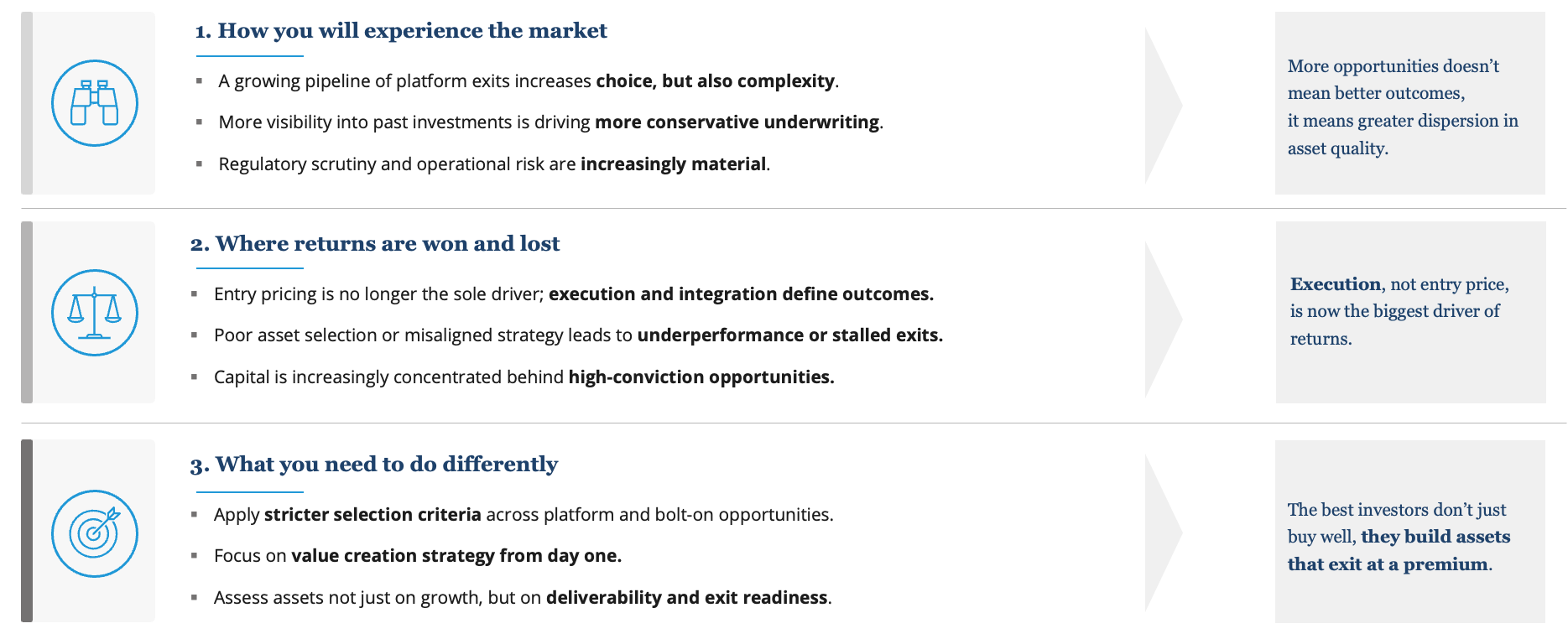

What This Means for Buyers and Investors

For buyers and investors, the evolving market creates both opportunities and risks, which is something that most founders, CEOs and investors underestimate. The increase in platform assets approaching exit is likely to create greater choice and potentially more attractive acquisition opportunities over time. At the same time, buyers will need to become increasingly sophisticated in assessing:

integration quality,

operational scalability,

management depth,

and strategic positioning.

The dispersion between strong and weak assets is likely to continue widening.

This makes the ability to identify businesses capable of sustaining premium positioning through future ownership cycles will become increasingly important.

Valuation Dispersion Will Continue Widening

One of the clearest signs of market maturity is widening valuation dispersion. This is where the market is quietly changing.

Recent transaction analysis from Dyer Baade & Company proprietary research demonstrates substantial spreads between lower quartile and upper quartile outcomes across:

EBITDA multiples,

revenue multiples,

and strategic platform valuations.

This is not temporary noise.

It is structural.

Premium businesses increasingly create:

strategic urgency,

buyer competition,

and asymmetric outcomes.

Average businesses increasingly struggle to differentiate themselves.

This is why firms with similar:

AUM,

revenues,

and EBITDA

can now achieve radically different outcomes.

So Will the Boom Continue?

That depends entirely on what people mean by “the boom.”

If the question is:

“Will wealth management remain one of the most attractive consolidation sectors in UK financial services?”

Then the answer is almost certainly yes.

The structural drivers remain exceptionally compelling:

fragmentation,

demographics,

recurring revenues,

regulation,

and operational scalability continue supporting long-term M&A activity.

But if the question is:

“Will all firms continue benefiting equally from broad market momentum?”

The answer is increasingly no.

The market is becoming:

more selective,

more institutional,

more quality-driven,

and much less forgiving.

This means:

premium businesses may continue achieving exceptional outcomes;

average businesses may increasingly struggle to command strong competition.

That is not the end of the boom.

It is the maturation of the market.

As the market matures, valuation outcomes are increasingly diverging between premium and average businesses. Our analysis on why similar wealth management firms now achieve radically different valuations can be found here.

Conclusion: The Winners Will Not Necessarily Be the Largest Firms

The UK wealth management M&A market remains one of the most attractive consolidation opportunities in European financial services.

But the nature of the market is changing fundamentally.

The next phase of the cycle will likely be defined less by:

broad valuation expansion

and more by:

strategic differentiation,

institutional quality,

operational scalability,

and future exit attractiveness.

The firms achieving the strongest outcomes in 2026 and beyond will not necessarily be the largest firms.

Increasingly, they will be the firms buyers believe are:

strategically important inside the next ownership cycle.

That is a very different market from the one that existed five years ago.

And the firms that recognise this shift earliest are likely to create the most value over the next decade.

About Dyer Baade & Company

Dyer Baade & Company advises founders, CEOs, and investors on wealth management M&A transactions across the UK mid-market, typically in the £20–200m valuation range. The firm combines strategic positioning with transaction execution to maximise valuation and deal certainty.

If you are considering a sale, assessing strategic options, or evaluating investment opportunities in the UK wealth management market, we would be happy to discuss your situation in confidence.