Why Private Equity Is Investing in UK Wealth Management Firms, and What It Means for Sellers and Investors

Introduction: Wealth Management Has Become a Core Private Equity Theme

Over the past decade, UK wealth management has evolved from a relatively niche consolidation story into one of the most active and institutionally recognised investment themes in European financial services.

Private equity firms are now deeply embedded across the sector. PE-backed consolidators have become major acquirers of IFAs and wealth managers, international investors are increasingly active in the UK market, and consolidation has accelerated materially across both advisory and discretionary wealth management.

This is not simply a UK phenomenon. Globally, private equity investment into asset and wealth management businesses has continued to increase sharply. According to recent S&P Global Market Intelligence research, global private equity-backed investments in asset management companies reached approximately $27.6bn in 2025, the highest level in more than five years and an increase of over 26% year-on-year. Aggregate transaction value has reportedly increased by approximately 340% since 2020.

The same structural drivers underpinning this global trend are highly visible in the UK market:

recurring revenues,

fragmentation,

demographic tailwinds,

regulatory-driven consolidation,

and scalable operating models.

For founders and shareholders of wealth management firms, this has created substantial opportunities. At the same time, it has fundamentally changed the dynamics of M&A processes, valuations, and buyer expectations.

For international private equity firms assessing the UK market, it has also created a highly attractive but increasingly sophisticated investment landscape in which local market knowledge, buyer positioning, and execution capability matter more than they did several years ago.

How Wealth Management Became a Key Investment Area for Private Equity in the UK

Historically, many private equity firms viewed wealth management with caution. The sector was often perceived as fragmented, heavily dependent on individual advisers, and difficult to scale operationally. Businesses frequently lacked institutional infrastructure, and recurring revenues were less established than they are today.

As a result, wealth management remained a relatively niche private equity strategy for many years.

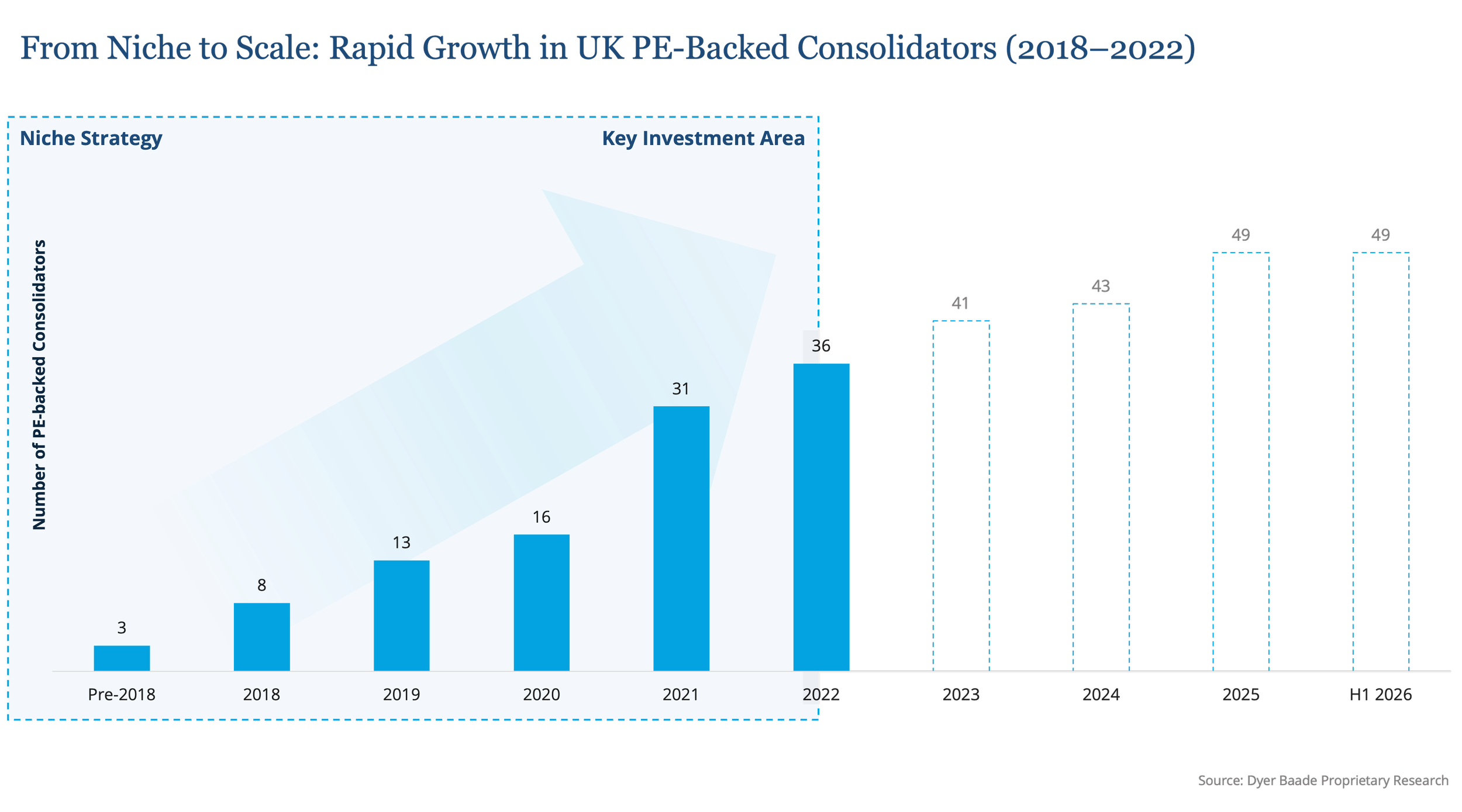

That began to change materially around 2018.

Several structural developments altered investor perceptions:

recurring fee-based revenue became more dominant;

regulatory frameworks matured;

technology improved scalability;

and wealth management firms increasingly professionalised their operations.

At the same time, the broader macro backdrop became increasingly attractive. Demographic shifts, growing private wealth levels, and the persistent advice gap created confidence that demand for wealth management services would remain structurally robust over the long term. The impact on private equity activity was significant. The number of PE-backed consolidators in UK wealth management increased rapidly over a relatively short period. What had once been considered a niche strategy evolved into one of the most proven buy-and-build themes within UK financial services.

Today, the market has reached a level of maturity where wealth management is no longer viewed as an “alternative” private equity strategy. It is increasingly treated as an established private equity sector focus.

Why Private Equity Firms Like Wealth Management

Private equity firms are ultimately searching for sectors that combine:

predictable cash flows,

fragmentation,

scalability,

defensiveness,

and multiple avenues for value creation.

UK wealth management increasingly offers all of these characteristics simultaneously.

Recurring Revenue and Predictable Earnings

One of the strongest attractions of wealth management is the quality of its revenue profile. Ongoing advice fees and discretionary management charges create recurring income streams that are substantially more predictable than revenues in many other industries. This creates visibility over future earnings and supports leveraged investment structures.

For private equity investors, recurring revenue is particularly attractive because it:

improves earnings predictability,

enhances financing capacity,

and supports long-term planning around value creation and exits.

Importantly, recurring revenue in wealth management is often linked to long-duration client relationships, creating a degree of resilience that institutional investors value highly. However, buyers are increasingly sophisticated in how they assess revenue quality. Firms with diversified client books, strong retention characteristics, and durable adviser relationships command materially greater interest than businesses where revenues appear recurring but remain operationally fragile. This increasing focus on quality is one of the reasons why valuation dispersion across the market has widened materially in recent years.

Fragmentation Creates a Long-Term Consolidation Opportunity

Another major attraction is the highly fragmented structure of the UK market. Despite years of consolidation activity, thousands of FCA-regulated advice firms continue to operate across the UK. A very large proportion of these businesses remain relatively small and founder-led, with over 85% currently operating with five advisers or fewer and an estimated 88 advice firms per consolidator, highlighting the depth of the consolidation opportunity.

For private equity firms, fragmentation creates a classic buy-and-build opportunity.

The strategy is straightforward in principle:

acquire a platform asset,

complete bolt-on acquisitions,

create operational efficiencies through scale,

improve margins,

and ultimately exit at a premium valuation multiple.

This consolidation model has proven highly attractive in practice and has become central to the sector’s investment thesis. Importantly, the opportunity remains substantial despite the amount of M&A activity already completed. While consolidation has clearly accelerated, the overall market remains highly fragmented relative to many other financial services sectors. This is one of the key reasons why international investors continue to view UK wealth management as attractive.

Demographic Tailwinds Remain Strong

The sector also benefits from exceptionally favourable long-term demographic dynamics. The UK population aged 65 and over is expected to grow materially over the coming decades, supporting long-term demand for:

retirement planning,

investment advice,

inheritance planning,

and wealth transfer services.

At the same time, private wealth levels continue to increase, particularly within affluent and high-net-worth demographics. Crucially, the sector still suffers from a substantial “advice gap.” A significant proportion of consumers with meaningful investable assets continue to operate without regulated financial advice, with only ~14% of addressable clients receiving advice. For private equity investors, this creates confidence that the underlying demand environment for wealth management services remains structurally attractive over the long term.

Regulation Is Accelerating Consolidation

Regulation has become another powerful driver of M&A activity. Increasing FCA requirements around:

compliance,

operational resilience,

reporting,

consumer duty,

and technology infrastructure

have materially increased the fixed-cost burden across the industry. These costs disproportionately affect smaller firms. Larger businesses are able to spread regulatory and operational costs across broader revenue bases, creating meaningful economies of scale. Smaller firms, by contrast, increasingly face pressure on profitability and operational capacity. This dynamic is accelerating consolidation. Private equity-backed platforms are particularly well-positioned to benefit because scale is central to their operating model. In many respects, regulation itself has become a structural driver of wealth management M&A.

Technology and Institutionalisation

Technology has further strengthened the investment case. Modern wealth management increasingly requires:

integrated CRM systems,

scalable reporting infrastructure,

compliance technology,

workflow automation (leveraging AI),

and sophisticated client engagement capabilities.

These investments require both capital and operational sophistication. Private equity-backed businesses are often able to deploy technology investments more effectively because they can leverage infrastructure across multiple acquisitions and operating entities. This has contributed to the broader institutionalisation of the sector. Increasingly, buyers favour businesses that demonstrate scalable operational models rather than purely relationship-driven structures. Operational robustness, management depth, and infrastructure quality now play a much greater role in buyer decision-making than they did earlier in the consolidation cycle.

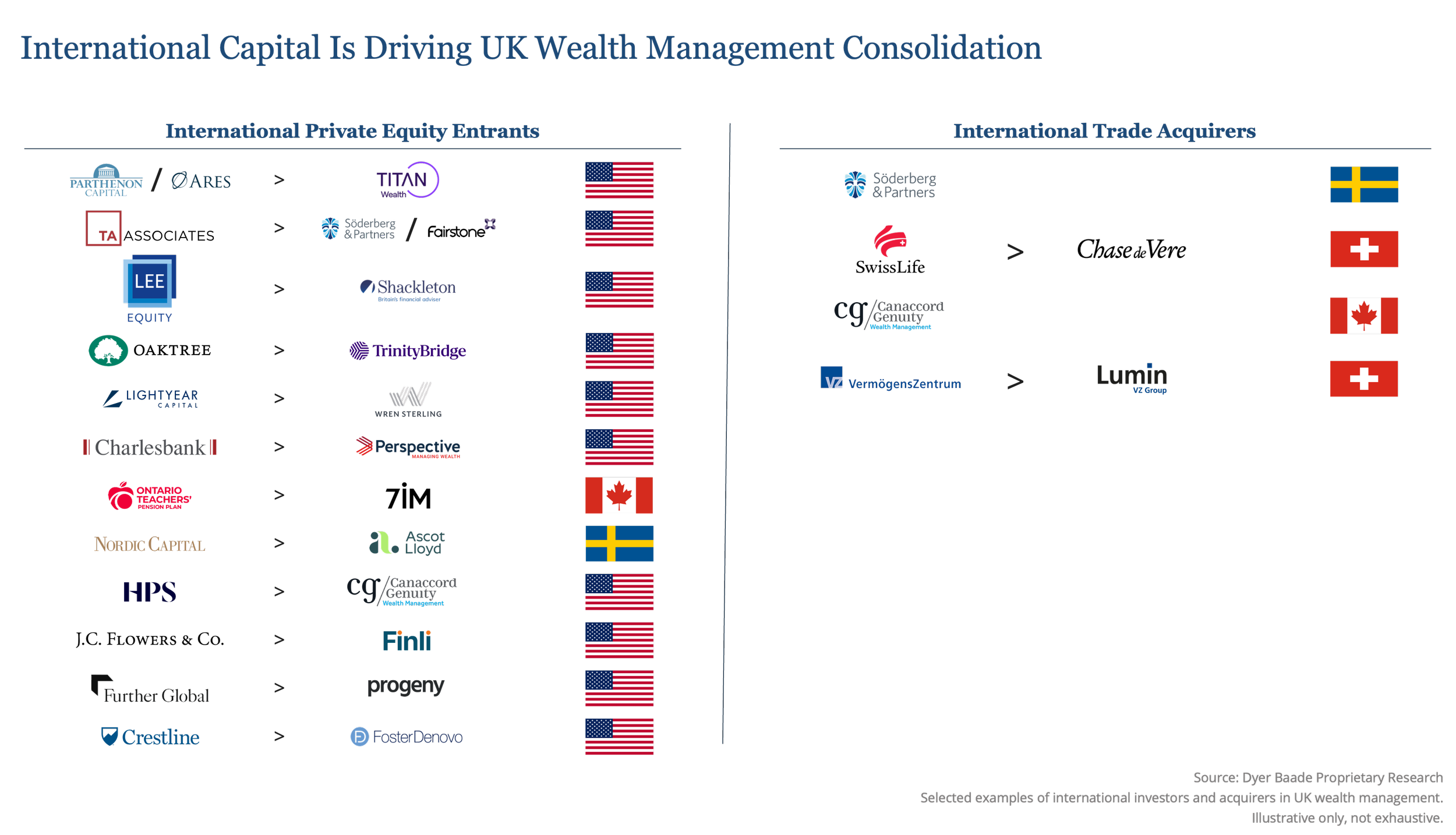

International Investors Are Increasingly Active in the UK Market

Another important development is the growing interest from international investors. Historically, UK wealth management consolidation was driven primarily by domestic private equity firms and UK consolidators. More recently, international investors have become increasingly active in the sector. This reflects growing recognition that the UK combines several highly attractive characteristics:

a large and sophisticated advice market,

strong recurring revenues,

deep fragmentation,

mature regulation,

and substantial consolidation potential.

For international PE firms, the UK wealth management sector increasingly represents one of the most scalable and mature consolidation opportunities in European financial services. However, it is also a market that requires deep understanding of:

buyer behaviour,

platform positioning,

integration dynamics,

regulatory nuances,

and competitive process management.

As the market becomes more sophisticated, execution capability and sector-specific expertise are becoming increasingly important differentiators. This is particularly relevant for international investors seeking to evaluate platform opportunities, assess bolt-on acquisition strategies, or navigate increasingly competitive sale processes.

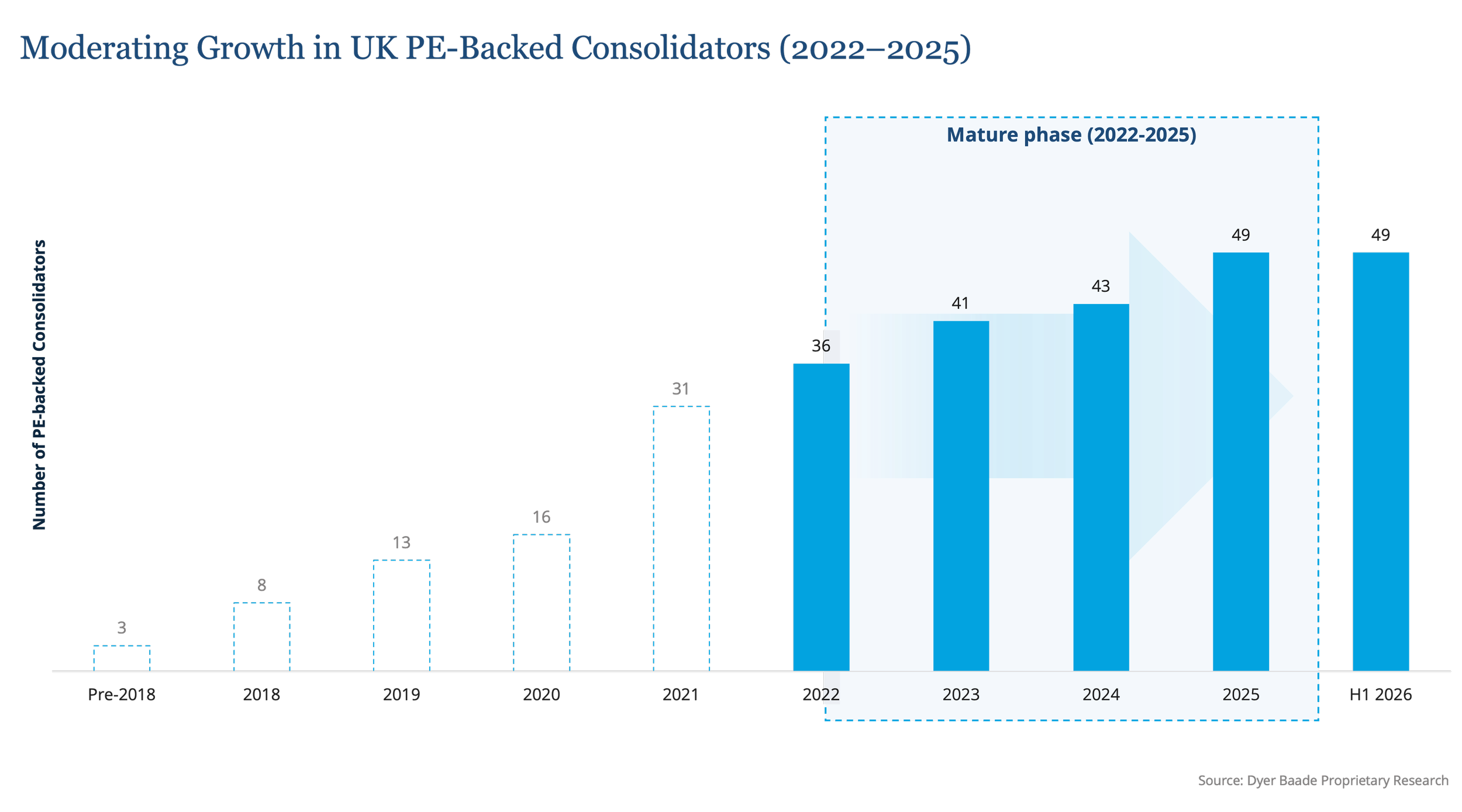

The Market Is Entering a More Mature and Selective Phase

While the long-term investment thesis remains highly attractive, the market itself is clearly evolving. The earlier phase of consolidation was characterised by:

rapid expansion,

strong capital inflows,

relatively limited supply of scaled assets,

and broad valuation momentum.

Today, the market is becoming more mature. A growing number of PE-backed consolidators are now reaching the stage at which they would typically seek an exit. Historically, only a relatively small number of scaled platform assets came to market in any given year. Going forward, that number is expected to increase materially. This shift matters because scarcity previously supported valuation premiums. As more assets compete for attention simultaneously, buyers have greater choice. Capital remains available, but it is becoming increasingly selective.

This has several implications:

buyers are conducting deeper diligence;

integration quality matters more;

execution risk receives greater scrutiny;

and valuation dispersion is widening materially.

The market has not stopped growing. However, it has clearly transitioned from a broad expansion phase into a more sophisticated selection phase.

Why Valuation Outcomes Are Diverging

As the market becomes more selective, valuation outcomes are diverging more noticeably, even among businesses of similar size. Buyers are increasingly differentiating between assets based on their ability to support platform growth, integration, and future exit potential. Premium assets continue to command strong valuations because they align closely with buyer strategies. Businesses that demonstrate scalability, operational robustness, strong management, and strategic relevance continue to attract significant competition. Average businesses, however, are increasingly treated as interchangeable. This distinction is important for both sellers and investors to understand.

Private equity buyers are no longer simply acquiring revenue streams. Increasingly, they are evaluating:

how a business strengthens a broader platform,

whether it improves future exit optionality,

and how it compares to competing opportunities in the market.

As a result, valuation is increasingly driven by:

strategic positioning,

scalability,

operational quality,

and integration capability.

What Private Equity Buyers Are Looking for Today

The profile of an attractive wealth management acquisition has evolved materially. Today, PE buyers are increasingly focused on:

strong recurring revenues,

institutional operating models,

diversified client books,

scalable infrastructure,

strong management teams,

and clear strategic differentiation.

Integration capability has also become critically important.

Earlier in the consolidation cycle, acquisition activity itself often drove enthusiasm. Today, buyers are increasingly focused on:

whether acquisitions genuinely create value,

whether integration has been successful,

and whether the business can support a premium exit in the future.

This increasing sophistication explains why some businesses continue to attract highly competitive valuations while others struggle to generate meaningful buyer tension.

What This Means for Sellers

For founders and shareholders considering a sale, the rise of private equity has fundamentally transformed the market.

The positive side is clear:

the buyer universe is broader,

international capital is increasingly active,

and demand for high-quality assets remains strong.

However, strong outcomes are no longer automatic. Businesses are increasingly being assessed relative to competing opportunities. Buyers want to understand not only the current quality of the business, but also:

how scalable it is,

how strategically relevant it is,

and how it fits within a broader platform strategy.

This means that positioning matters materially more than it did several years ago.

Figure 1: What this means for Owners of

firms with <£1bn AUM

Figure 2: What this means for Owners of

firms with £1bn+ AUM

Figure 3: What this means for Shareholders & Management of Private Equity backed firms

Strategic vs Incremental: The Key Distinction

One of the most important concepts in the current market is whether a business is viewed as strategic or incremental.

Strategic businesses provide a clear solution to a buyer’s objectives. This may include:

geographic expansion,

attractive client demographics,

strong organic growth,

scalable infrastructure,

or acquisition integration capability.

Incremental businesses are typically treated as bolt-ons. Importantly, this distinction is not determined solely by size. A well-positioned medium-sized business may attract significantly more interest than a larger but undifferentiated firm. This is one of the key reasons why valuation outcomes are becoming increasingly polarised across the market.

Why Preparation Matters More Than Ever

As the market becomes more sophisticated, preparation increasingly determines outcomes. Private equity buyers are conducting deeper diligence and assessing businesses through a much more institutional lens than in previous years. Well-prepared businesses typically:

articulate a stronger strategic narrative,

engage more effectively with the right buyers,

preserve valuation during diligence,

and maintain stronger competitive tension throughout the process.

Poorly prepared businesses often experience:

elongated timelines,

weaker engagement,

greater buyer leverage,

and valuation pressure late in the process.

In today’s market, premium outcomes are increasingly engineered before a process formally begins.

The Outlook for Private Equity in UK Wealth Management

Despite increasing selectivity, the long-term outlook for private equity investment in UK wealth management remains highly positive. The core investment thesis remains intact:

recurring revenues,

demographic tailwinds,

fragmentation,

regulatory-driven consolidation,

and scalable operating models continue to support the sector.

At the same time, the next phase of the market is likely to be materially more sophisticated than the last. Private equity firms are increasingly prioritising:

quality,

scalability,

operational execution,

and strategic positioning.

As a result, the strongest outcomes are likely to concentrate around businesses that combine strong fundamentals with clear strategic relevance and robust execution capability.

Conclusion: Private Equity Has Permanently Reshaped the UK Market

Private equity has fundamentally transformed UK wealth management. What began as a niche consolidation strategy has evolved into a mature institutional investment theme supported by long-term structural drivers and increasingly global pools of capital. This transformation has created major opportunities for:

founders considering exits,

management teams seeking growth capital,

and international investors looking to build or expand UK platforms.

At the same time, the market has become more competitive, more institutional, and more selective. Today, buyers are assessing businesses not simply on current earnings, but on strategic relevance, scalability, operational quality, and future exit potential. For both sellers and investors, understanding this shift is now essential, irrespective of the fact, that the future outlook for UK wealth management M&A remains strong.

About Dyer Baade & Company

Dyer Baade & Company advises founders, CEOs, and investors on wealth management M&A transactions across the UK mid-market, typically in the £20–200m valuation range. The firm combines strategic positioning with transaction execution to maximise valuation and deal certainty.

The firm also advises domestic and international investors on acquisitions and platform-building strategies within the UK wealth management sector.

If you are considering a sale, evaluating strategic options, or assessing investment opportunities in the UK market, we would be happy to discuss your situation in confidence.