How to Value a Wealth Management Firm in the UK (2026) - Multiples, Methodologies & Key Drivers

The Market Is No Longer Paying for Participation

Most founders still believe wealth management valuation is primarily a function of:

AUM,

EBITDA,

or market conditions.

That is increasingly wrong.

The UK wealth management M&A market has fundamentally changed over the last several years. The era in which almost every decent business benefited from rising consolidation momentum is ending. The market is no longer paying premium valuations simply because a firm exists within an attractive sector.

Today, the market is dividing into two categories:

businesses buyers need;

businesses buyers can easily replace.

That distinction is now driving valuation outcomes far more than headline scale metrics.

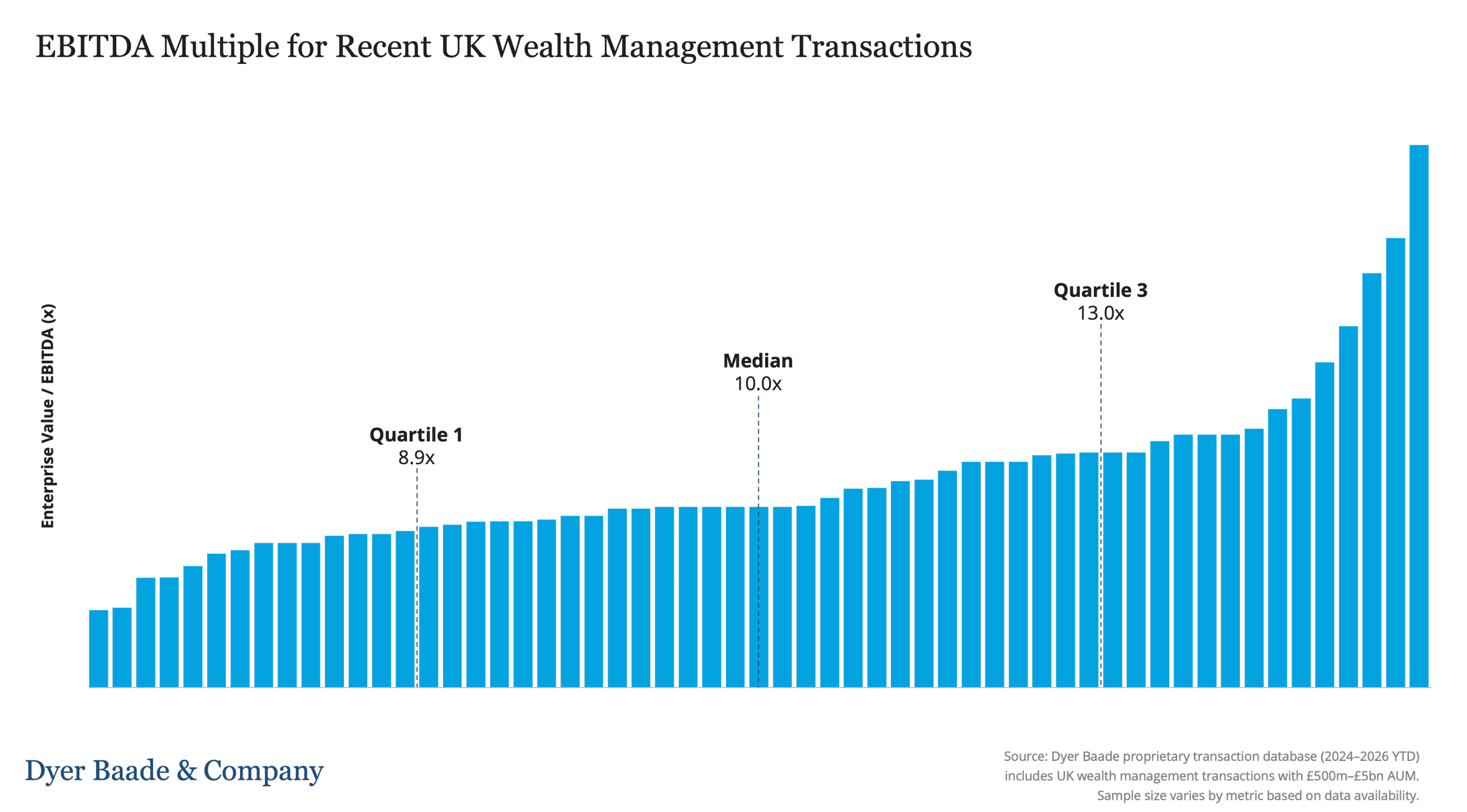

Recent UK transaction data from Dyer Baade & Company proprietary research illustrates the point clearly:

lower quartile EBITDA multiples currently sit around 8.9x;

median transactions are around 10.0x;

upper quartile outcomes reach approximately 13.0x;

while exceptional strategic assets are achieving materially higher valuations.

That spread is not noise.

It is the market signalling that buyers are no longer pricing businesses uniformly.

In practical terms, two firms with similar AUM and similar revenues can now achieve valuation outcomes that differ by 50–100% or more.

Why?

Because valuation is no longer primarily a financial exercise. It is increasingly a strategic one.

While this article explains how wealth management firms are valued, valuation outcomes in practice are increasingly diverging. Our analysis on why similar firms achieve radically different valuations can be found here.

Part I: Multiples - Why “Market Multiples” Are Becoming Misleading

The Biggest Mistake Founders Make

The single biggest mistake founders make is asking: “What multiple are firms trading at?” Sophisticated buyers do not think this way. There is no longer one “wealth management multiple.”

There is:

a premium tier for strategically relevant assets;

a broad middle market of operationally acceptable firms;

and a lower tier of businesses that buyers increasingly view as commoditised.

The valuation gap between these groups is widening rapidly. This is why generic benchmarking has become dangerous.

EBITDA Multiples: The Market’s Real Language

EBITDA remains the dominant institutional valuation metric because it reflects what sophisticated buyers actually care about:

cash generation,

scalability,

integration potential,

and future exit optionality.

Recent UK transaction data from Dyer Baade & Company’s proprietary UK wealth management transaction database shows:

Quartile 1: 8.9x EBITDA

Median: 10.0x EBITDA

Quartile 3: 13.0x EBITDA

However, the most important number is not the median. It is the spread. A market with tight valuation ranges implies broad agreement on quality. A market with wide dispersion implies something different: buyers are aggressively differentiating between businesses. That is exactly what is happening today.

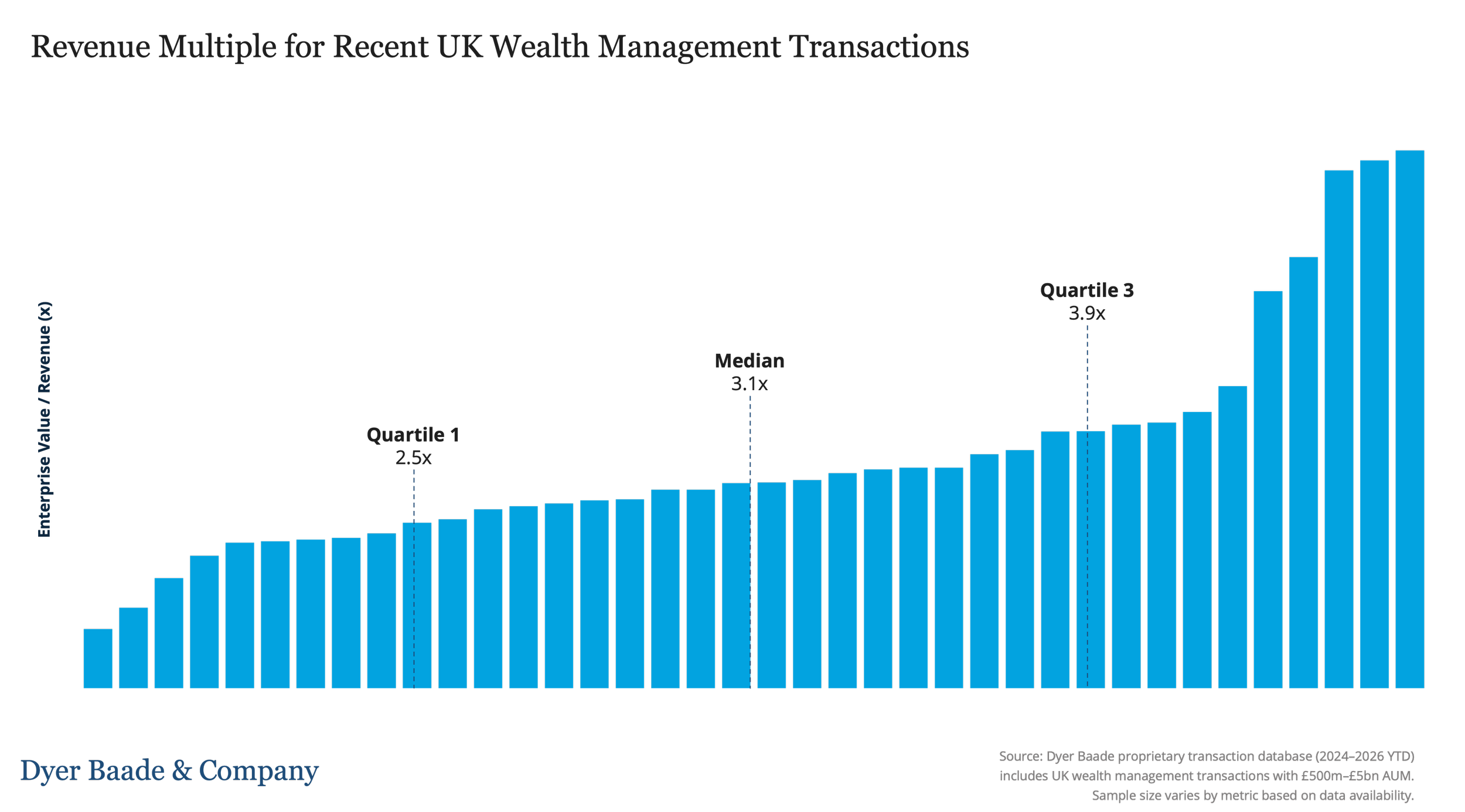

Revenue Multiples: Quality Is Starting to Dominate Quantity

Revenue multiples increasingly reveal how buyers perceive revenue durability.

Current UK transaction data indicates:

Quartile 1: 2.5x revenue

Median: 3.1x revenue

Quartile 3: 3.9x revenue

Again, the spread matters more than the midpoint. Sophisticated buyers increasingly distinguish between:

recurring and transactional revenue;

scalable and founder-dependent revenue;

durable and vulnerable revenue.

In earlier phases of consolidation, many businesses benefited from broad market optimism. Today, buyers are underwriting retention risk much more aggressively. That changes valuation materially.

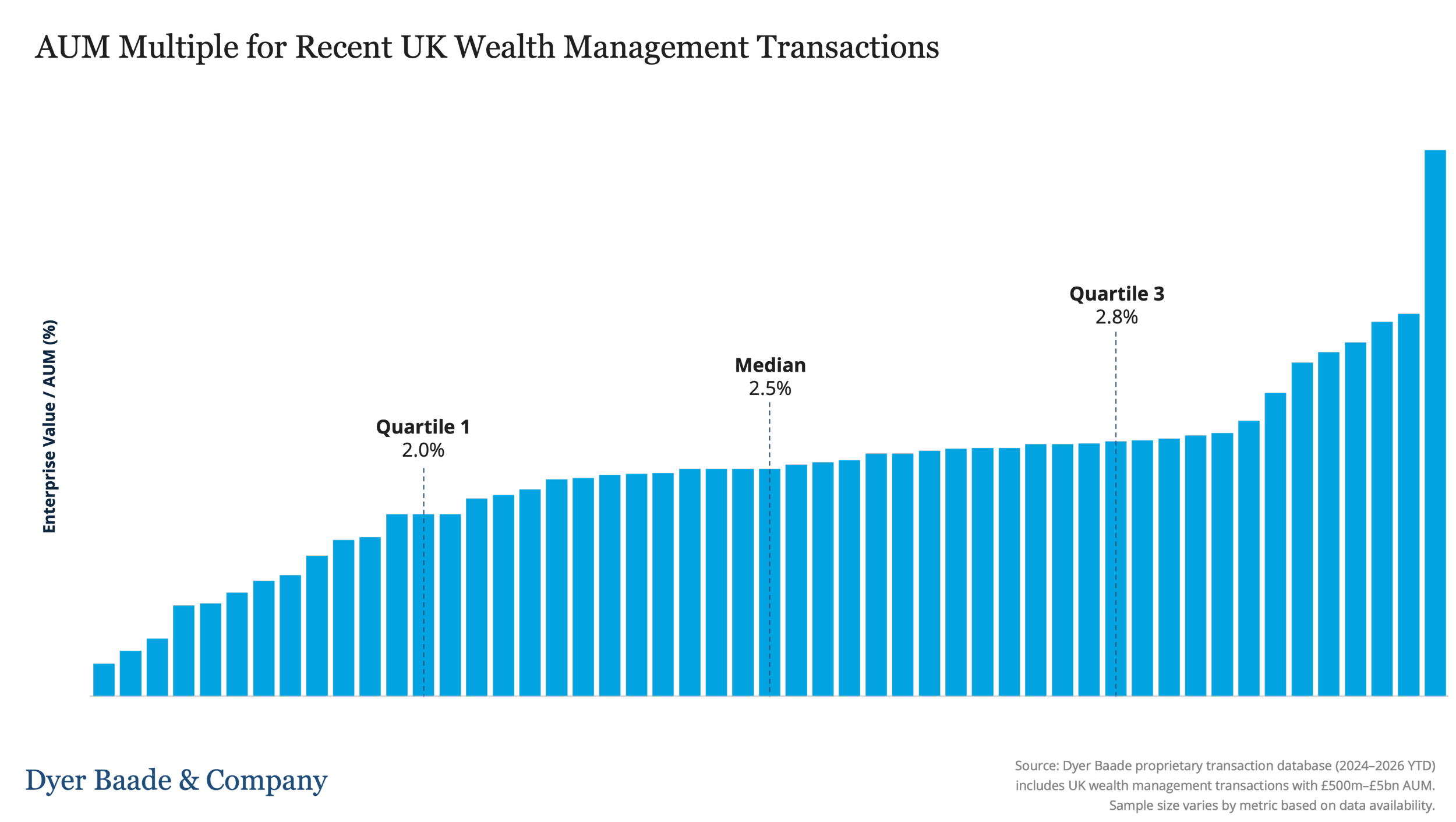

AUM Multiples: Why Lazy Buyers Still Use Them

AUM multiples remain widely discussed because they are easy to understand. That does not mean they are sophisticated. Current UK transaction data from Dyer Baade & Company proprietary research covering UK wealth management transactions between 2024–2026 YTD shows:

Quartile 1: 2.0% of AUM

Median: 2.5% of AUM

Quartile 3: 2.8% of AUM

The problem is obvious: AUM alone tells you almost nothing about economic quality. The market is finally recognising this properly. £1bn of low-retention advisory assets is not equivalent to £1bn of high-margin discretionary mandates with institutional infrastructure. Sophisticated buyers know this. Unsophisticated sellers often do not.

Part II: Methodologies - How Sophisticated Buyers Actually Think

Buyers Do Not “Value” Businesses. They Price Risk and Strategic Relevance.

This is one of the most misunderstood concepts in wealth management M&A. Most founders believe valuation is a mathematical exercise. Institutional buyers understand that valuation is primarily:

a risk pricing exercise,

combined with a strategic relevance exercise.

That distinction changes everything.

EBITDA Methodology: Why Institutional Buyers Prefer It

Private equity firms and sophisticated consolidators prefer EBITDA because EBITDA reflects:

operational scalability,

financing capacity,

and future exit potential.

However, the critical point is this: buyers are not valuing historical EBITDA. They are valuing: future sustainable institutional EBITDA.

That is why “normalisation adjustments” matter so much. Buyers will aggressively analyse:

owner remuneration,

operational inefficiencies,

non-recurring costs,

revenue durability,

and scalability.

The quality of the EBITDA matters far more than the headline number itself.

Revenue Methodology: Why It Still Matters

Revenue-based valuation remains particularly important within:

founder-led IFAs,

hybrid businesses,

and firms where profitability is operationally distorted.

However, buyers increasingly segment revenues with extreme sophistication. The market is becoming much harsher toward:

transactional income,

concentrated client books,

and founder-dependent revenues.

Meanwhile, businesses with:

highly recurring revenues,

younger client demographics,

and strong retention metrics

continue to command premium pricing. This is why simplistic “industry averages” are becoming increasingly meaningless.

Why Sophisticated Buyers Triangulate

The best buyers rarely rely on one valuation framework. They triangulate between:

EBITDA,

revenue,

AUM,

operational scalability,

integration complexity,

and future exit potential.

Why?

Because the real question is not: “What is this business worth today?”

The real question is: “What could this business become inside our platform?”

That is what drives premium outcomes.

Part III: Key Drivers - What Actually Separates Premium Assets

The Market Is Rewarding Institutional Quality

The UK wealth management sector is institutionalising rapidly. This is one of the most important developments in the market.

Historically, many firms were effectively collections of adviser relationships. Today, sophisticated buyers increasingly want:

scalable infrastructure,

management depth,

operational consistency,

and transferable client relationships.

The market is no longer rewarding personality-driven businesses the way it once did. That shift is structural, not cyclical.

Revenue Quality Is Becoming Ruthlessly Important

In a tighter capital environment, recurring revenue quality matters enormously. Sophisticated buyers increasingly analyse:

retention durability,

adviser dependency,

client demographics,

fee sustainability,

and concentration risk.

This is one reason why valuation dispersion is widening. As highlighted repeatedly in Dyer Baade & Company’s proprietary market analysis, the gap between premium and average outcomes in UK wealth management M&A is no longer marginal - it is becoming structurally significant.

The market is increasingly pricing resilience, not just growth.

Strategic Relevance Is Now the Real Multiplier

The highest valuations increasingly go to businesses that solve a strategic problem. These businesses are not simply “good firms.” They are strategically useful firms. For example:

businesses enabling geographic expansion,

firms with scalable infrastructure,

platforms with strong integration capability,

or firms attractive to future secondary buyers.

These assets create competition. Competition creates valuation asymmetry. That is where premium outcomes come from.

The Era of Generic Consolidation Is Ending

The market is now mature enough that buyers are becoming much more selective.

Earlier in the cycle, almost any acquisition contributed to platform growth narratives.

Today, buyers increasingly ask:

does this acquisition genuinely improve the platform?

does it improve future exit optionality?

can it scale operationally?

will future buyers pay a premium for this asset?

This is a much more sophisticated market than the one that existed five years ago.

Conclusion: Valuation Is Becoming a Strategic Discipline

The UK wealth management M&A market is no longer behaving like a simple consolidation story. It is becoming a strategic capital allocation market. That distinction matters enormously. Today, premium outcomes increasingly go to firms that combine:

institutional quality,

scalable infrastructure,

recurring revenues,

strategic relevance,

and strong positioning.

Average businesses may still transact. But the gap between average and exceptional outcomes is widening rapidly. In many respects, the market is no longer asking:

“How big is this business?”

The market is increasingly asking:

“How strategically valuable is this business inside the next ownership cycle?”

That is the question sophisticated buyers are pricing today, and increasingly, it is the only valuation question that truly matters.

About Dyer Baade & Company

Dyer Baade & Company advises founders, CEOs, and investors on wealth management M&A transactions in the UK mid-market, typically in the £20–200m valuation range. The firm combines strategic positioning with transaction execution to maximise valuation and deal certainty.

If you are considering a sale or would like to understand how your business would be valued in today’s market, we would be happy to discuss your position in confidence.