Why Similar Wealth Management Firms Achieve Radically Different Valuations in 2026

The Market Didn’t Slow Down. It Split.

For many years, valuation discussions in UK wealth management were relatively straightforward. A business with a certain level of Assets Under Management (AUM), recurring revenue and profitability could generally expect to achieve a valuation within a reasonably predictable range. While individual transactions always differed, buyers often applied broadly similar frameworks when assessing value.

That is no longer the case.

Today, two firms with remarkably similar financial profiles can achieve dramatically different outcomes. One may attract multiple competing bidders and command a premium valuation. The other may struggle to generate meaningful buyer interest despite having comparable AUM, revenues and EBITDA. This widening gap has become one of the defining characteristics of the UK wealth management M&A market in 2026. Importantly, this is not because buyers have disappeared. Private equity interest remains strong. Strategic acquirers remain active. Capital remains available, but it is becoming more selective. This increasing selectivity reflects broader structural shifts in UK wealth management M&A.

The reason is different. Buyers have become significantly more selective. The market has not slowed down. It has split.

In this article, we examine why valuation outcomes are diverging, the factors driving this trend, and what founders and shareholders can do to position themselves for a premium outcome.

For a technical breakdown of valuation methodologies, EBITDA multiples and AUM-based valuation frameworks, see our guide to valuing wealth management firms.

The Myth: Similar Firms Should Achieve Similar Valuations

One of the most common misconceptions among founders is that valuation is largely determined by a handful of financial metrics. The logic appears straightforward. If two firms have similar: AUM, revenues, EBITDA and adviser numbers, then they should achieve broadly similar valuations.

In practice, that assumption is increasingly wrong.

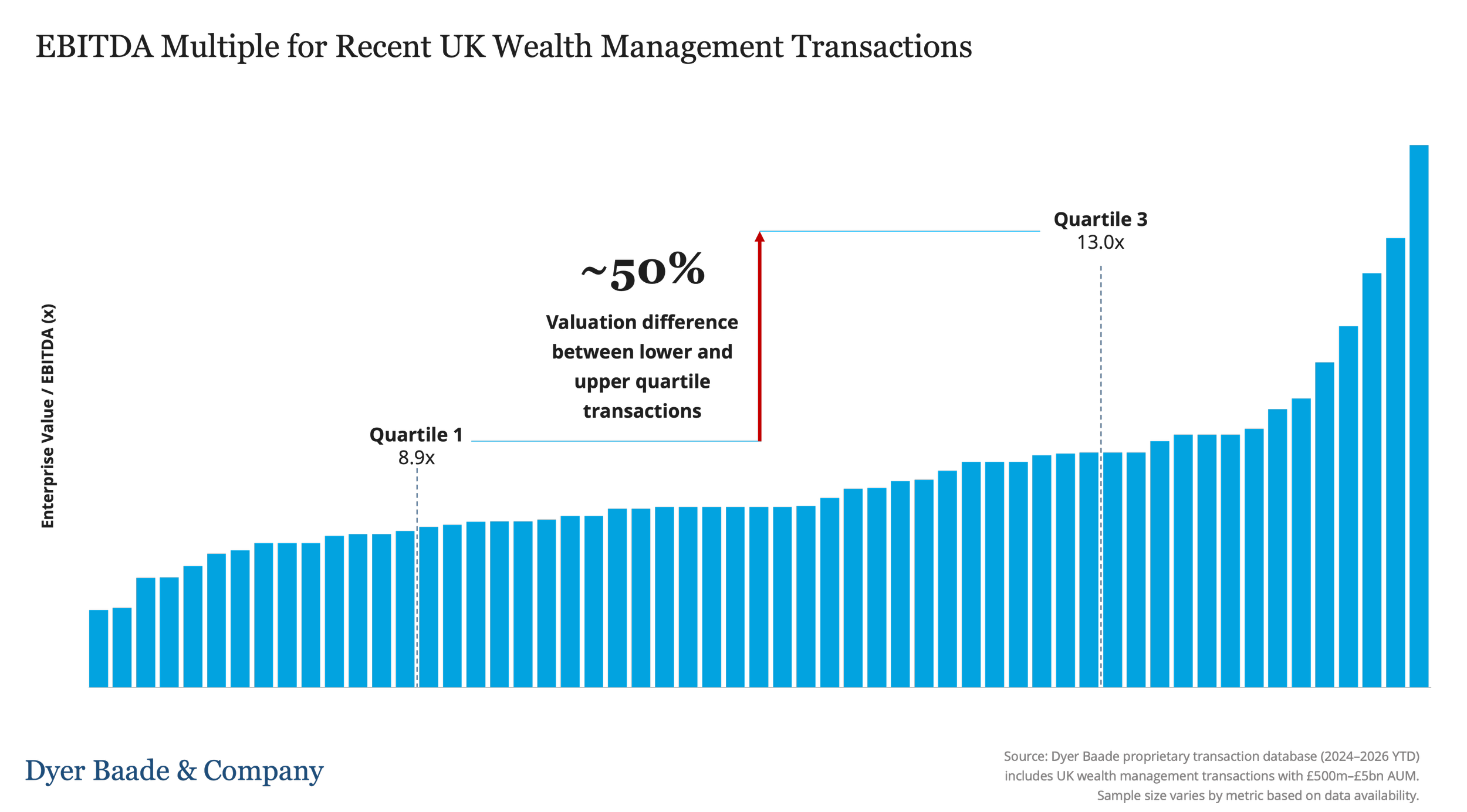

Recent transaction data demonstrates a substantial spread between lower-quartile and upper-quartile valuation outcomes across the wealth management sector. While average EBITDA multiples remain attractive by historical standards, premium businesses continue to achieve significantly stronger outcomes than their peers.

The implication is clear. The market is no longer valuing businesses solely on what they are today. It is increasingly valuing them on what buyers believe they can become.

As a result, valuation has become as much a strategic question as a financial one.

The Five Drivers of Valuation Dispersion

If financial performance alone no longer explains valuation outcomes, what does?

Based on Dyer Baade & Company's proprietary research and experience advising on more than 40 wealth management transactions, five factors are increasingly driving the gap between average and premium outcomes.

1. Strategic Positioning

Perhaps the most important driver of valuation is strategic relevance. Buyers are no longer simply asking: "Is this a good business?" Increasingly, they are asking: "Why is this business more valuable than the alternatives available to us?" A firm with a clear market position, differentiated client proposition or attractive niche can often generate substantially more buyer interest than a broadly similar generalist competitor. The most valuable businesses are often those that solve a strategic problem for the buyer.

2. Management Depth and Founder Dependency

Founder-led businesses can be highly successful. However, buyers increasingly place a premium on businesses that can thrive without the founder. A management team capable of driving growth, integrating acquisitions and operating independently reduces risk and improves scalability. Two businesses may generate identical profits today. The business with stronger management depth often commands the higher valuation.

3. Scalability and Infrastructure

As the sector matures, buyers are placing greater emphasis on operational robustness. Areas receiving increasing scrutiny include:

technology infrastructure

compliance frameworks

reporting capabilities

operational processes

integration readiness

Institutional-quality businesses tend to attract more interest because they offer greater confidence around future growth and integration.

4. Revenue Quality

Not all recurring revenues are viewed equally. Buyers increasingly assess:

client retention rates

adviser retention

revenue concentration

client demographics

fee sustainability

The quality and predictability of future cash flows often matter more than the absolute level of current earnings.

5. Buyer Fit

Valuation is ultimately determined by what a specific buyer is willing to pay. A business that perfectly fits a buyer's acquisition strategy can attract a significantly stronger valuation than a business with similar financial characteristics but less strategic relevance.

This explains why competitive tension remains one of the most powerful drivers of value creation.

Why Is The Gap Widening Now?

The obvious question is: Why is this valuation gap becoming more pronounced? In our view, the answer lies in the evolution of the market itself. Over the last decade, wealth management has attracted substantial private equity investment. Numerous consolidators have been established, scaled and institutionalised. As a result, the market has become considerably more sophisticated. The number of PE-backed consolidators has increased significantly, while the overall volume of bolt-on acquisition opportunities has remained relatively stable.

This has created a very different dynamic from the one that existed five or ten years ago. Earlier in the consolidation cycle, many buyers were still seeking exposure to the sector. Today, many already have it. As more PE-backed platforms mature and approach potential exit events, buyers are increasingly comparing multiple opportunities simultaneously. They have more choice, more data and more benchmarks than ever before. The consequence is greater selectivity. Capital remains available, but it is increasingly concentrated behind businesses that demonstrate scalability, strategic relevance and future exit potential.

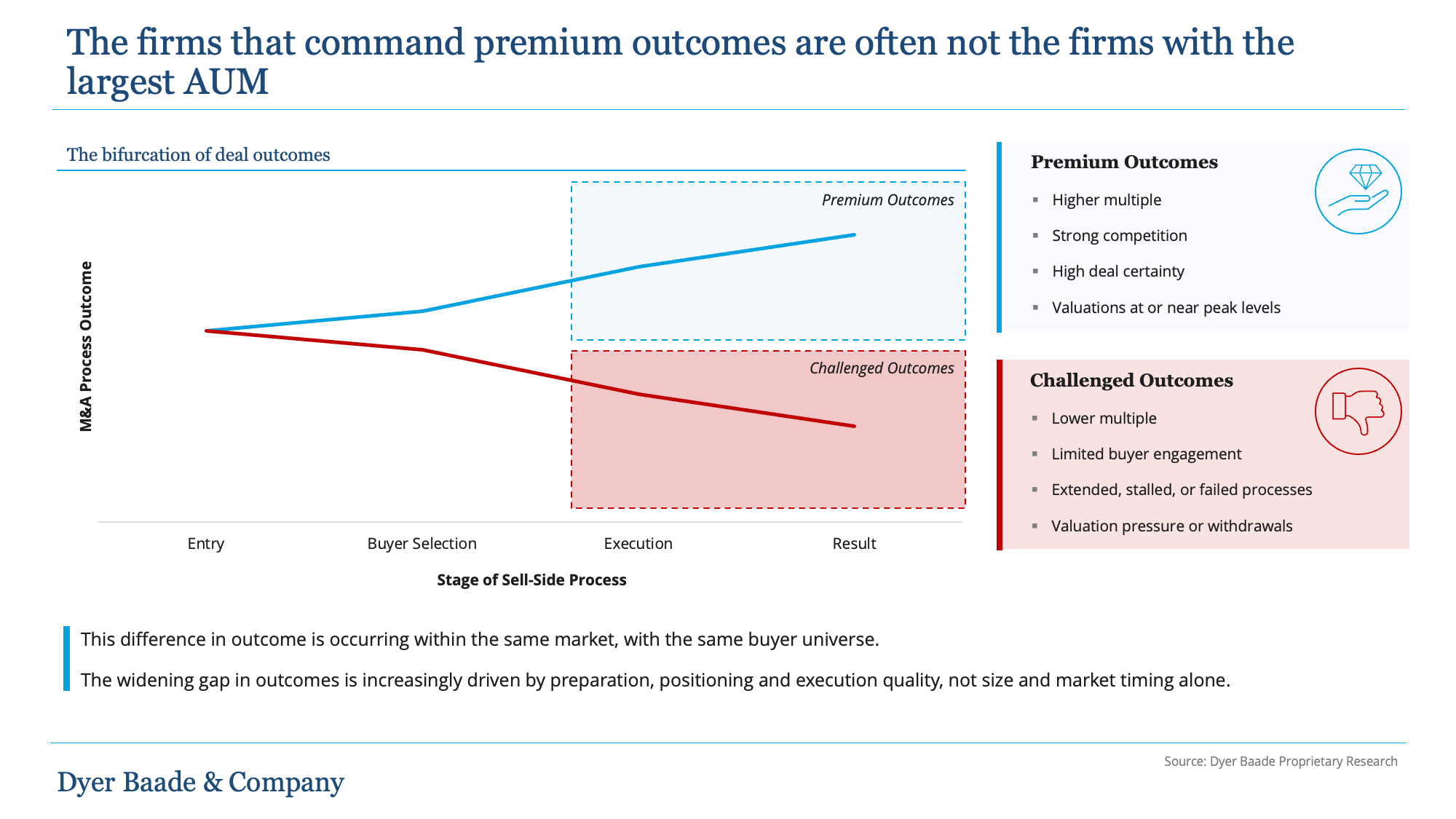

The Emergence of the Outcome Gap

One way to think about today's market is through what we describe as the "Outcome Gap". At one end of the spectrum are businesses that are well positioned, scalable and strategically attractive. These firms continue to attract strong buyer interest and often achieve valuations close to peak market levels. At the other end are businesses that may have respectable financial performance but lack clear differentiation. These firms increasingly struggle to generate competitive tension and are more likely to face valuation pressure. Importantly, the gap between these groups appears to be widening. The market is not becoming weaker. It is becoming more discriminating.

Case Study: Similar Firms, Different Outcomes

Consider two hypothetical firms. Both manage approximately £1 billion of client assets. Both generate similar revenues and EBITDA. Both operate within the same regulatory environment. Yet one business achieves a materially higher valuation. Why?

The first business has:

a strong management team;

low founder dependency;

scalable infrastructure;

attractive client demographics;

and a clear acquisition strategy.

The second relies heavily on its founder, has limited management depth and lacks a compelling strategic narrative. Financially, they may appear similar. Strategically, they are very different. Buyers recognise this distinction and increasingly price accordingly.

How to Move From Average to Premium

The encouraging news for founders is that many of the factors driving valuation can be improved. The businesses that consistently achieve premium outcomes tend to focus on:

strengthening management depth;

reducing founder dependency;

improving operational scalability;

enhancing reporting and governance;

clarifying strategic positioning.

Importantly, these initiatives often create value regardless of whether a sale ultimately occurs. As the market becomes more selective, preparation is becoming an increasingly important valuation driver. The strongest outcomes are rarely created during the transaction process itself. They are usually created years before the business comes to market.

The Importance of Adviser Selection

An often underappreciated driver of valuation outcomes is the structure of the sale process itself.

To state the obvious, transactions do not occur in a vacuum. The way a business is brought to market: whether through a fully advised process, a broker-led approach, or on an unadvised basis, has a direct influence on both valuation and deal certainty.

Fully advised processes tend to be more structured, more competitive, and more rigorously managed. They typically involve detailed preparation, targeted buyer engagement, and disciplined control of process dynamics. This often results in stronger competitive tension, more robust diligence outcomes, and, ultimately, higher valuation and greater execution certainty.

By contrast, unadvised transactions are more likely to be opportunistic in nature. They may involve a narrower buyer universe, less formal positioning, and more limited competitive dynamics. As a result, outcomes can be more variable and, on average, less optimal from a valuation and certainty perspective.

Broker-led processes typically sit somewhere between these two extremes. While they can facilitate access to buyers and support transaction execution, they often lack the depth of preparation, strategic positioning, and process management associated with fully advised mandates. This can lead to less consistent outcomes, particularly in more complex or competitive situations.

It is also important to recognise that not all “advice” is equal. There is a meaningful distinction between informal intermediation, independent advisory, and institutional, FCA-regulated advisory delivered by professional firms. As the market has become more sophisticated, buyers have increasingly responded to this distinction. Processes that are well-prepared, professionally managed, and institutionally credible are more likely to attract high-quality buyers and sustain pricing through diligence.

Importantly, the impact of adviser-led processes is not uniform across the market. At smaller deal sizes, where transactions are more transactional and less institutional, the difference between process types is often less pronounced. However, as deal size increases to the £20m - £200m valuation range and transactions become more complex, the role of a structured, well-executed process becomes increasingly important. In this context, adviser involvement should not be viewed simply as a transactional facilitator. Rather, it is a key component of how businesses are positioned, marketed, and ultimately valued within a more selective and competitive market environment.

About Dyer Baade & Company

Dyer Baade & Company advises founders, CEOs, and investors on wealth management M&A transactions across the UK mid-market, typically in the £20–200m valuation range. The firm combines strategic positioning with transaction execution to maximise valuation and deal certainty.

If you are considering a sale or would like to understand how your business would be positioned in today’s market, we would be happy to discuss your situation in confidence.