Trust Companies vs Fund Administrators vs Corporate Services Firms: Why Valuations Differ and How Owners of Mid-Sized Businesses Can Benefit from the Differences

A few months ago, a trust company owner asked me a simple question. A friend of his had recently sold a fund administration business. Both businesses generated similar profits. Both operated in respected offshore jurisdictions. Both had strong management teams. Yet the fund administration business reportedly achieved a materially higher valuation.

His question was straightforward: "Why?"

It is one of the most important questions in the sector, because at first glance many trust companies, fund administrators and corporate services providers look remarkably similar. They often operate in the same jurisdictions. They are regulated by the same authorities. Many employ similar people. Many even sit in the same office buildings in Jersey, Guernsey or Luxembourg. Yet buyers frequently value them very differently.

The reason is that buyers are not purchasing today's profits. They are purchasing tomorrow's profits, and the future looks very different depending on whether your clients are wealthy families, international corporates or private equity fund managers.

Understanding this distinction is often the difference between an average transaction outcome and an exceptional one. More importantly, it helps explain why some businesses consistently achieve premium valuations while others struggle to do so. The answer has surprisingly little to do with EBITDA. It has far more to do with the type of client sitting on the other side of the table.

Three Markets Hiding Inside One Industry

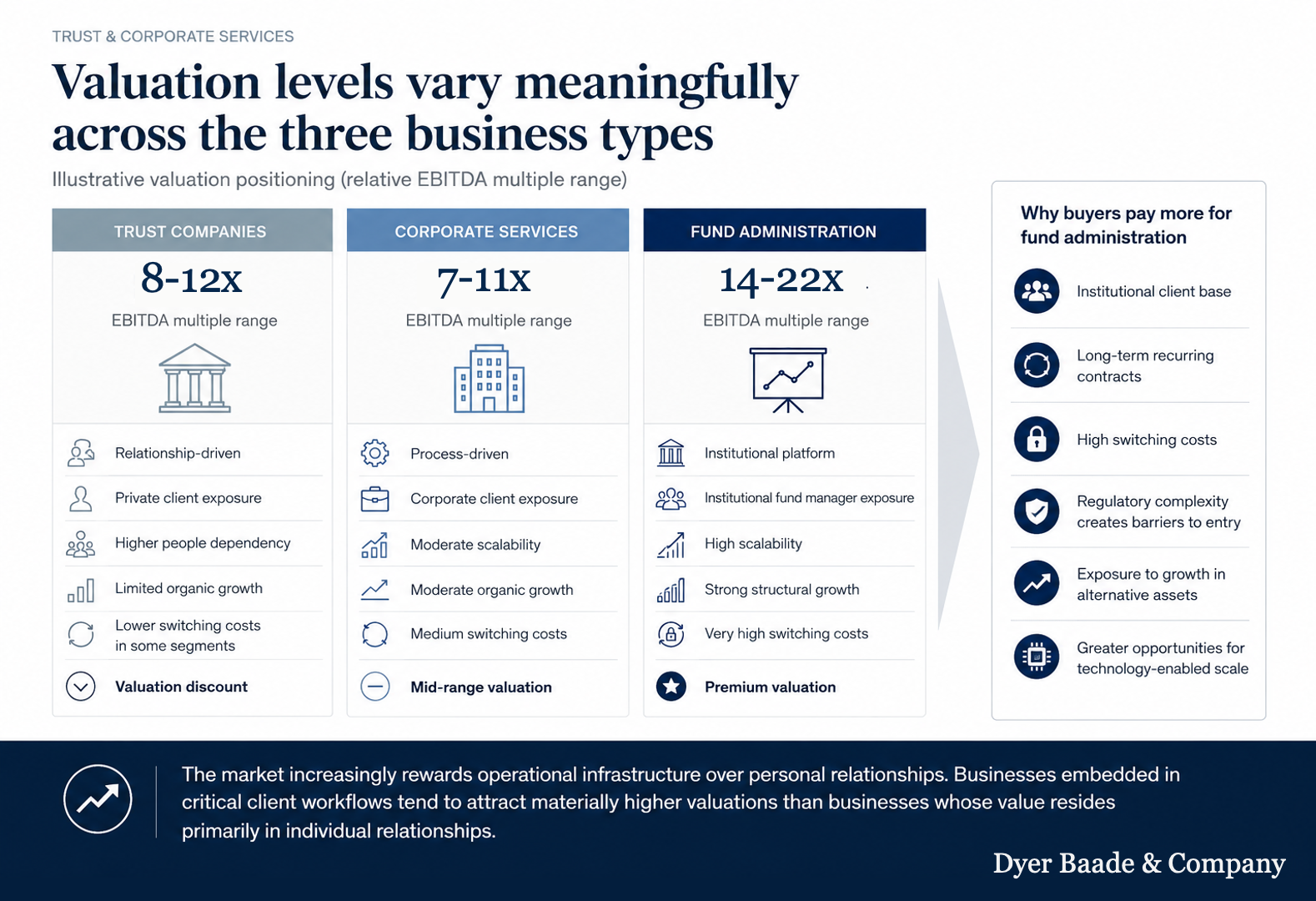

The trust and fiduciary sector is often spoken about as though it were a single market. It is not. In reality, it consists of three distinct business models. The first serves private clients through trusts, foundations, family structures and fiduciary arrangements. The second serves international corporates through company administration, governance and corporate services. The third serves institutional investors through fund administration. The businesses frequently overlap.

Many firms offer services across multiple categories. Yet the underlying economics are very different. The clients behave differently. The switching costs differ. The growth profiles differ. The technology requirements differ.

Most importantly, the way buyers think about value differs. This is why a trust company, a corporate services business and a fund administrator can generate identical profits but receive very different valuations.

Why Trust Companies Are Really Relationship Businesses

Most trust company owners instinctively understand where their value comes from. It is not technology. It is not scale. It is not administration. It is trust. A family may remain with the same fiduciary adviser for twenty years. Sometimes thirty. Sometimes across multiple generations.

Over time the trustee becomes involved in major family decisions, succession planning, governance matters and wealth preservation strategies. The relationship becomes embedded. This creates exceptionally resilient revenues. However, it also creates a challenge. Who does the client trust? The institution? Or the individual?

This question sits at the heart of most trust company transactions. Many founders underestimate how heavily buyers focus on it. A trust company generating £4 million of EBITDA may appear highly attractive. However, if buyers conclude that the founder personally owns most of the client relationships, they become nervous.

What happens when the founder leaves? Will the clients stay? Will the next generation of management retain the same level of trust? These concerns directly influence valuation. Conversely, a trust company that has successfully institutionalised relationships often attracts significantly stronger offers.

The irony is that many founders believe their personal involvement increases value. In reality, it can sometimes suppress it. The businesses that achieve the strongest outcomes are often those where clients trust the organisation as much as they trust any individual within it.

Why Fund Administration Often Sits at the Top of the Valuation Range

If one studies many of the larger transactions completed across the sector over the past decade, fund administration businesses frequently command some of the highest valuation multiples. This is not an accident. The economics are fundamentally different. Consider a private equity fund. The typical life cycle is ten to twelve years. Infrastructure funds are often longer. Private credit structures can also extend over many years. Once a fund administrator has been appointed, replacing them becomes expensive, disruptive and operationally risky.

As a result, retention rates tend to be exceptionally high. This creates something buyers value enormously: Visibility. A fund administrator frequently knows where a substantial portion of its revenues will come from several years into the future. Very few professional services businesses can say the same. Yet the real attraction goes beyond visibility.

The strongest fund administration businesses benefit from a powerful flywheel. A private equity manager launches Fund I. The administrator performs well. Three years later the manager launches Fund II. The administrator is retained. Then comes Fund III. Then Fund IV. Assets under management increase. Complexity increases. Fee income increases. One client relationship can generate revenues for decades.

This is why sophisticated buyers spend considerable time analysing the quality of the underlying fund managers. In many respects, they are underwriting the future success of those managers as much as the administrator itself. A client roster populated by growing private equity firms with strong fundraising records is often worth materially more than one populated by managers with limited future growth.

This explains why seemingly similar fund administrators can achieve very different valuations. The market is not paying for administration. It is paying for future fund launches.

Why Corporate Services Is Being Re-Rated

Corporate services is perhaps the most misunderstood part of the sector. Historically it was often regarded as the least exciting segment. The work was administrative. The services were process-driven. Margins were frequently lower. Many observers assumed technology would gradually reduce its value. The opposite may be happening.

Artificial intelligence is reducing the value of administration. It is increasing the value of client ownership. This distinction matters enormously.

Imagine two businesses. The first has one hundred wealthy families as clients. The second has three thousand active corporate clients. Historically, investors focused on the fees generated from those relationships. Increasingly, they focus on the opportunities created by those relationships. A corporate client requiring company administration today may require trust structures tomorrow. It may require governance services. It may require fund administration. It may require support entering new jurisdictions.

The administrative relationship becomes a distribution channel.

This is precisely why many of the larger international platforms have spent years broadening their service offerings. Once a trusted relationship exists, expanding services becomes significantly easier than acquiring entirely new clients. As a result, corporate services businesses are increasingly being viewed as strategic client-acquisition platforms rather than administrative providers. That shift in perception has important implications for valuation.

Why Geography Matters More Than Many Founders Realise

Another common mistake is to assume that local buyers determine value. Increasingly they do not. Twenty years ago, a Jersey trust company was usually sold to another Jersey trust company. Today, the buyer may be based in Luxembourg, Zurich, New York or Singapore.

The reason is strategic relevance. A Luxembourg platform may want Channel Islands capabilities. A Swiss group may seek access to UK-related structures. An American acquirer may view a European trust business as a gateway into an entirely new market. The value of a business therefore depends not only on what it does but also on who is looking at it.

This is one reason why cross-border M&A has become such a powerful driver of valuation. The same business can look completely different depending on the buyer's strategic objectives. To a local competitor, a Guernsey trust company may represent additional scale. To an international buyer, it may represent entry into an entire jurisdiction. Those are very different acquisition rationales. And very different rationales frequently produce very different valuations.

What The Largest Transactions Teach Us

Many independent business owners dismiss the sector's largest transactions as irrelevant. This is understandable. A twenty-person trust company in Jersey has little in common with a multinational platform operating across dozens of jurisdictions. Yet the largest transactions reveal how sophisticated buyers think. Businesses such as JTC, IQ-EQ, Ocorian, TMF, Intertrust and Tricor did not achieve scale by accident. Nor did investors allocate billions of pounds to the sector because administration is exciting. They invested because they recognised several important trends.

The first is that regulatory complexity continues to increase.

The second is that technology investment is becoming more important.

The third is that clients increasingly want broader capabilities across multiple jurisdictions.

The fourth is that recurring revenues remain highly attractive.

These trends continue to drive consolidation.

However, there is another lesson that receives less attention. The most successful acquirers are not necessarily those that integrate most aggressively. Across the industry there are examples where acquisitions looked compelling on paper but failed to deliver the expected outcome. Key employees departed. Clients left. The culture that originally made the business successful disappeared. The lesson is simple. Scale creates advantages, but preserving relationships remains critical.

A buyer who misunderstands this can destroy value remarkably quickly. For founders considering succession, that distinction matters. The highest offer is not always the best offer.

How Mid-Sized Firms Can Benefit

Many owners look at the industry's largest platforms and conclude that they cannot compete. That is usually the wrong conclusion. The objective is not to become a smaller version of a global consolidator. The objective is to understand what buyers reward. Trust companies can improve management depth and succession planning. Fund administrators can broaden client relationships and service offerings. Corporate services firms can strengthen client retention and cross-selling opportunities.

The most attractive businesses increasingly combine characteristics from multiple sectors. The relationship strength of a trust company. The earnings visibility of a fund administrator. The client access of a corporate services platform.

These are precisely the attributes that buyers consistently reward. Importantly, none of them require a business to become significantly larger. They require a business to become more transferable, more resilient and more strategically relevant.

The Real Determinant of Value

After many years of transactions across the trust, fiduciary and broader financial services sectors, one observation consistently proves true. Valuation is ultimately a reflection of confidence. Confidence that clients will remain. Confidence that revenues will grow. Confidence that management can operate without the founder. Confidence that the business will be more valuable five years from now than it is today.

The sectors differ. The business models differ. The valuation multiples differ.

Yet the underlying principle remains remarkably consistent. Buyers do not pay premium valuations because a business performed well in the past. They pay premium valuations because they believe it will perform well in the future.

Understanding what creates that confidence is often the first step towards building a more valuable business, and ultimately, that is the lesson that trust companies, fund administrators and corporate services firms can all learn from one another.

Considering your Strategic Options?

Dyer Baade & Company is an independent M&A advisory firm specialising in transactions across financial and professional services, including wealth management, trust and fiduciary businesses, typically in the £20–200m valuation range. The firm combines strategic positioning with transaction execution to maximise valuation and deal certainty.

If you are considering a transaction, succession plan or strategic partnership within the next five years, we would be pleased to discuss your objectives in confidence.