Mergers & Acquisitions in the Art Market

Executive summary

The art market is not undergoing a conventional consolidation cycle. Galleries remain fragmented, founder-dependent and culturally resistant to corporate ownership, while the most active M&A is occurring around the infrastructure that makes art easier to sell, finance, value, insure, transport and administer. Auction houses are expanding vertically into private sales, advisory, lending, data and luxury goods; private equity is assembling regional auction platforms; and investors are acquiring art logistics, software and market-intelligence businesses with more transferable revenues than traditional dealerships.

The central thesis is therefore not simply that art-market M&A is increasing. It is that capital is selectively institutionalising the art ecosystem: consolidation is strongest where businesses control recurring revenue, proprietary data, transaction flow, physical infrastructure or trusted compliance capabilities, and weakest where enterprise value remains inseparable from a founder’s relationships and judgement.

Dr. Daniel Baade, formerly Head of Strategy and Global Strategy Director at Christie’s and now CEO of Dyer Baade & Company, argues that the distinction is fundamental. “The art market is unlikely to consolidate evenly,” he says. “The businesses most capable of attracting institutional capital are not necessarily those closest to the artist. They are those that can turn an opaque, episodic and relationship-driven market into something more searchable, financeable and administratively manageable—without destroying the trust on which it depends.” Baade’s former Christie’s roles and current position at Dyer Baade are publicly described in his professional profile and the firm’s corporate materials.

Research methodology

This analysis reviews material developments between approximately 2011 and July 2026, with greater weight given to transactions completed or announced since 2018. It draws principally on corporate announcements, regulatory filings, public-company disclosures, government guidance and leading market reports, supplemented by established financial and specialist art-market publications where transaction details were not disclosed directly.

The absence of a comprehensive global database for acquisitions of privately held galleries, advisers, logistics companies and art-technology businesses is an important limitation. Deal counts and aggregate M&A values cannot therefore be stated reliably. The analysis instead uses a verified transaction sample to identify where capital has been deployed, what types of buyers are active and which strategic rationales recur. Transaction values are described as disclosed, reported estimates or undisclosed; no undisclosed values have been inferred.

Market context: large, global and unusually cyclical

The global art market generated estimated sales of $59.6 billion in 2025, an increase of 4 per cent after two successive years of declining values. Dealer sales rose by 2 per cent to $34.8 billion, public-auction sales increased by 9 per cent to $20.7 billion, and reported private sales by auction houses declined by approximately 5 per cent to just under $4.2 billion. The number of transactions increased by only 2 per cent, to an estimated 41.5 million.

The recovery should not be mistaken for a return to broad-based exuberance. In 2024, sales had fallen by 12 per cent to $57.5 billion, with weakness concentrated at the top end of the market. The contrast between falling aggregate value and greater resilience at lower price points illustrated a defining characteristic of the sector: a small number of trophy transactions can materially alter annual market totals, while the much larger volume of modestly priced transactions follows a different cycle.

The art market is therefore large but structurally unlike most consumer or luxury markets. It is not a single industry with standardised products and transparent unit volumes. It is a collection of overlapping primary and secondary markets covering fine art, decorative art, antiquities, design, photography and adjacent collectibles. Each object is heterogeneous; supply at the top end is discretionary; comparable pricing is imperfect; and sellers often withdraw works rather than accept a visibly disappointing price.

This creates pronounced operating leverage. Auction houses invest in specialists, premises, technology and global marketing before knowing whether owners will consign the works required to cover those costs. Dealers carry inventory, fund artists and exhibitions, attend expensive fairs and wait for transactions that can be unpredictable in timing. When confidence weakens, high-value sellers may simply decline to sell, depriving intermediaries of both revenue and price discovery.

The same cyclicality complicates corporate valuation. Revenue can rise sharply when a business secures one major collection or estate, but that income may not recur. A record year may reflect exceptional consignments rather than sustainable market-share gains. Conversely, a weak year may reveal market conditions rather than a deteriorating franchise. Buyers must therefore distinguish structural earnings from transaction volatility more carefully than in most professional-services or luxury businesses.

M&A activity overview: selective institutionalisation, not wholesale consolidation

There is no robust public measure of global art-market M&A. Many businesses are privately owned, consideration is commonly undisclosed and smaller transactions may be structured as asset purchases, partnerships, team moves or inventory transfers rather than conventional share acquisitions.

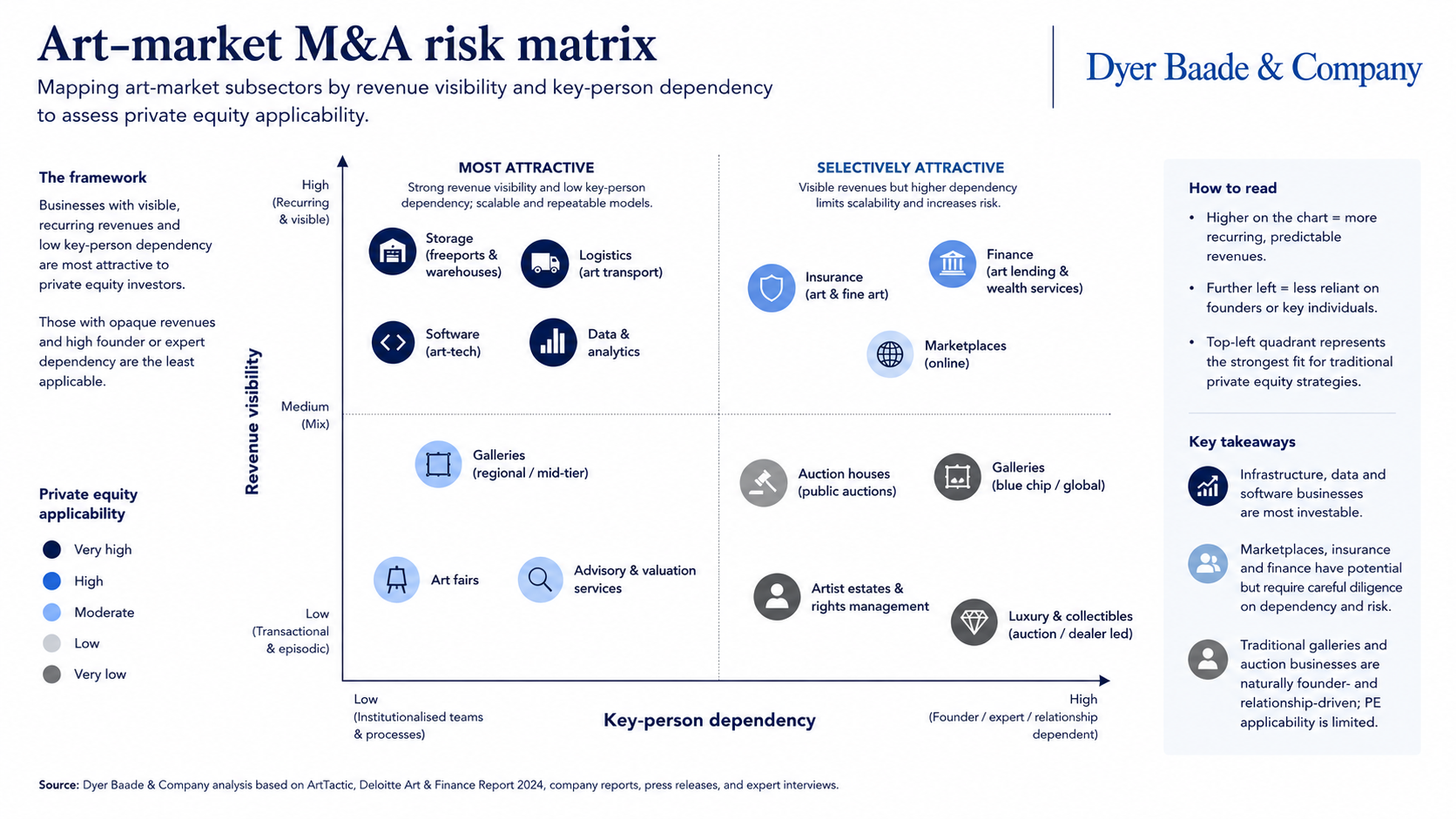

The available transaction evidence nevertheless shows a clear pattern. Art-market M&A is concentrated around businesses that can achieve scale without commoditising the art itself: auction platforms, logistics, storage, data, software, lending, valuation and collection administration.

These businesses offer at least one of four attributes attractive to institutional buyers:

recurring or repeat revenue;

proprietary market or object data;

physical or digital infrastructure;

control over transaction flow or collector relationships.

Traditional galleries offer fewer of these qualities. Their value may depend on the continuing loyalty of artists and collectors, neither of which is always contractually protected. A gallery can own a prestigious name, valuable inventory and an enviable client list yet still have limited transferable enterprise value if its founder is the principal originator of artists, consignments and sales.

This makes art-market M&A different from consolidation in accountancy, wealth management or insurance broking. In those sectors, client revenues are generally recurring, service delivery can be standardised and relationships often survive a change of ownership. In art, a buyer may acquire the legal entity while losing the people, artists or collectors that made it valuable.

“The central transaction question is not simply what the company earned last year,” says Baade. “It is which part of those earnings belongs to the business and which part belongs personally to the founder, specialist or consignor relationship. That distinction determines whether a buyer is acquiring an institution or renting a network.”

Subsector analysis

Auction houses: from auctioneers to integrated client platforms

Auction houses have been the most important consolidators because they sit at the intersection of supply, demand, data, finance and advice. Their core public-auction business provides price discovery and brand visibility, but its revenue is episodic and dependent on obtaining high-quality consignments.

The leading houses have consequently expanded into private sales, lending, valuation, estate advisory, luxury goods and digital commerce. Sotheby’s has also acquired advisory, data, scientific-analysis and image-recognition capabilities. This is vertical integration: the objective is to participate in more stages of the collector’s ownership cycle, from acquisition and finance to collection management and eventual disposal.

Bonhams has pursued a more conventional buy-and-build strategy under Epiris. Its acquisitions of Bukowskis, Bruun Rasmussen, Skinner and Cornette de Saint Cyr created a network of established regional houses with local brands and sourcing relationships. Bonhams confirmed the four acquisitions in its corporate materials; financial terms were not disclosed.

The strategic rationale is powerful. Regional houses often possess loyal clients and specialist expertise but lack global marketing, technology and cross-border distribution. A scaled owner can centralise selected functions while retaining local identities. The execution risk is equally clear: excessive integration could cause the very specialists and consignors that justified the acquisition to leave.

Galleries: expansion without conventional consolidation

The gallery sector remains structurally fragmented. Even internationally prominent galleries have generally expanded by opening branches, recruiting specialists and adding artists rather than acquiring competitors.

The reasons are commercial as much as cultural. Artist relationships may be non-exclusive. Collector information can reside in personal address books rather than institutional systems. Inventory values are subjective. A founder’s curatorial judgement may be inseparable from the brand, while artists and clients can react negatively to a change in ownership.

Pace Gallery’s 2022 combination with Los Angeles-based Kayne Griffin demonstrates the circumstances in which a gallery acquisition can make strategic sense: a desirable geographic presence, established premises, an experienced team and compatible artistic relationships. The consideration was not disclosed. The transaction was closer to acquiring an embedded cultural platform than executing a conventional cost-synergy merger.

Gallery consolidation is therefore likely to remain selective. Succession-driven transactions, team acquisitions, joint ventures and acquisitions of estates or archives are more plausible than a large-scale roll-up of dealer businesses.

Online platforms: strategic relevance, difficult economics

Online channels have permanently changed art-market distribution but have not displaced physical inspection, personal recommendation or specialist trust. Global online art sales fell to $9.2 billion in 2025 after the pandemic-era acceleration, although they remained materially above pre-2020 levels.

Platforms provide clear value in search, discovery, remote bidding, price comparison and lower-value transactions. Their strategic difficulty is monetisation. Collectors and dealers can discover one another online and subsequently transact privately, preventing the platform from capturing the full economics of the relationship.

1stDibs’ 2021 flotation illustrated investor appetite for a scaled digital marketplace. The company priced 5.75 million shares at $20, implying gross offering proceeds of $115 million before costs. Its earlier acquisition—and later disposal—of Design Manager also demonstrated the attraction and limitations of software adjacency: workflow products can deepen engagement, but they must be sufficiently integrated with the marketplace to justify ownership.

The collapse of Auctionata and Paddle8 provides the counterexample. Their 2016 merger promised global online scale; Auctionata entered insolvency proceedings in 2017, and Paddle8 later filed for Chapter 11. The lesson is not merely that growth was too expensive. It is that client-money discipline, consignor trust and cash conversion matter more than gross merchandise value.

Art technology and data: from optional tools to strategic infrastructure

Art-market technology is shifting from front-end marketplaces towards the infrastructure used by professionals: collection-management systems, pricing databases, inventory tools, provenance records, image recognition and compliance workflows.

The 2025 takeover of Artnet by Leonardo Art Holdings is strategically significant for this reason. The offer was €11.25 per share, representing an approximately 97 per cent premium to the specified unaffected share price. The buyer ultimately secured approximately 98.93 per cent of Artnet and completed its delisting from the Frankfurt Stock Exchange.

Artnet’s value lies not only in advertising or editorial traffic but in its historical auction-price database, market brand and network of buyers and professionals. Data of this kind can support valuations, lending, insurance, advisory and business development.

The merger of Winston Art Group and Artory applies a related thesis. It combines appraisal expertise and advisory services with collection data and secure portfolio tools. The resulting business describes itself as serving collectors, fiduciaries and institutions and states that its predecessor appraisal operation had assessed more than $100 billion of art and collectibles. These are company-reported claims, but the strategic direction is clear: expert judgement is being combined with scalable information infrastructure.

Logistics and storage: the strongest natural roll-up thesis

Fine-art logistics may offer the most conventional consolidation opportunity in the art ecosystem. It combines recurring storage fees with barriers to entry including secure premises, climate control, insurance, customs expertise, trained handlers and international transport networks.

Iron Mountain’s ownership and expansion of Crozier illustrates the model. In 2018, Crozier acquired Artex Fine Arts Services, adding five facilities, customer relationships and more than 160,000 square feet of US storage capacity.

Scale can create tangible synergies: higher utilisation of specialist facilities and fleets, broader geographic coverage, shared technology, stronger procurement and the ability to serve museums, galleries, auction houses and collectors across jurisdictions. Unlike a gallery, the service is not wholly dependent on one individual’s taste or personal standing.

The risk is that operational failure can destroy reputation quickly. Damage, loss, customs errors or confidentiality breaches can impair a logistics brand built over decades. Acquirers must preserve technical expertise and risk controls rather than treating the target as conventional warehousing.

Insurance and risk management: strategically adjacent, transaction-light

Art insurance is commercially important but less visible as a standalone M&A category. Much activity sits within large insurers, specialist underwriting units and brokerage groups rather than independent art businesses.

Its strategic importance is increasing because insurance depends on many of the same assets sought elsewhere in the value chain: reliable valuations, condition reports, ownership data, location records and claims history. The 2025 strategic partnership between AXA XL and Winston Artory Group, for example, links insurance and cultural-asset protection with appraisal and collection information. It was a partnership rather than an acquisition.

Potential acquisition opportunities are more likely to arise in specialist brokerage, valuation technology, risk analytics and collection-management services than in large underwriting carriers.

Art finance: attractive relationships, demanding collateral controls

Art-backed lending has strategic value to auction houses, private banks and specialist credit providers. It allows collectors to release liquidity without selling and can give a lender access to broader wealth-management relationships or future consignments.

But art is difficult collateral. Title can be disputed, authenticity questioned and liquidation periods prolonged. Public sales may reveal distress, while private enforcement across jurisdictions can be legally and reputationally complex.

Fractional-ownership platform Masterworks extends the financialisation thesis further by offering securities linked to special-purpose entities holding artworks. SEC disclosures explicitly warn investors that artworks are illiquid, may fall in value, may not appreciate sufficiently to cover fees and may face authenticity, physical-damage and artist-specific market risks.

This is commercially meaningful innovation, but it does not eliminate the underlying illiquidity of art. It repackages exposure and provides a regulated distribution mechanism.

Key deal case studies

1. Sotheby’s: a trophy take-private becomes a strategic recapitalisation

Patrick Drahi’s BidFair acquired Sotheby’s in 2019 for an enterprise value of approximately $3.7 billion. The transaction paid $57 per share and returned the company to private ownership after more than three decades as a listed business.

The strategic case for private ownership was that Sotheby’s required capital and flexibility to compete across guarantees, property, technology, lending and luxury categories without being assessed against quarterly public-market expectations.

The model also carried balance-sheet risk. In 2024, ADQ agreed to acquire a minority stake as part of approximately $1 billion of new investment alongside Drahi. ADQ stated that the proceeds would reduce leverage and support growth; its financial statements subsequently recorded a 24.18 per cent ordinary-share stake, acquired for AED2.049 billion, alongside convertible preference shares and warrants.

This was more than a capital injection. It broadened Sotheby’s buyer universe from entrepreneurial private ownership to sovereign-backed strategic capital and strengthened its connection to Abu Dhabi’s growing cultural and luxury economy.

The case demonstrates both the attraction and the capital intensity of a global auction platform. Brand, data and client access can justify exceptional strategic value, but guarantees, real estate, lending and cyclical auction revenues require patient shareholders.

2. Bonhams: private equity’s clearest art-market roll-up

Epiris acquired Bonhams in 2018 and subsequently supported a series of acquisitions, most notably the four regional auction houses acquired in 2022.

The thesis resembles a classic platform-and-bolt-on strategy. Each target brought a local brand, consignor relationships, specialist departments and regional sourcing. Bonhams brought international distribution, technology, marketing and the opportunity to route important objects to the venue most likely to maximise price.

This model is more viable than a gallery roll-up because auction-house revenues are linked to transactions rather than long-term representation of artists. Regional brands can also be retained rather than eliminated.

The principal deal risk is specialist retention. If senior experts leave after integration, the buyer may discover that it acquired premises and a trade name but not the relationships that generated consignments.

3. Artnet: data becomes a control asset

The 2025 Artnet takeover is one of the strongest recent examples of investors attributing strategic value to art-market information.

Leonardo Art Holdings’ €11.25-per-share offer represented a substantial premium and was supported by Artnet’s management and supervisory boards. The buyer described private ownership under a stable, long-term shareholder as central to the strategic rationale.

Artnet demonstrates why data businesses can attract a wider buyer universe than traditional art intermediaries. Historical transaction records are relevant to auction houses, advisers, lenders, insurers, collectors and wealth managers. Once standardised and integrated into professional workflows, the data can generate subscription revenue and improve other services.

The challenge is that auction results are not a complete record of the art market. Private sales, gallery transactions, withdrawn lots and differences in condition or provenance limit the predictive value of comparable prices. The asset is therefore most powerful when combined with expert interpretation.

4. Crozier and Artex: industrial logic enters the art world

Iron Mountain’s development of Crozier shows how an industrial strategic buyer can identify value in art-market infrastructure.

The acquisition of Artex added facilities and clients in major US art centres. The synergies were practical rather than speculative: denser transport routes, greater storage capacity, broader geographic coverage and the ability to cross-sell logistics, installation and collection services.

The model also benefits from revenue visibility. Storage contracts can generate recurring income even when auction volumes fall. This contrasts with transaction-led businesses whose income depends on collectors deciding to sell.

For private equity and infrastructure-minded strategic buyers, art storage is consequently more legible than art dealing. The physical assets, occupancy, customer concentration and capital expenditure can be diligenced using familiar frameworks, although specialist handling and reputation remain critical.

5. Auctionata and Paddle8: the danger of mistaking activity for enterprise value

The Auctionata–Paddle8 merger was intended to create a global online auction leader. Instead, Auctionata entered insolvency proceedings within a year and Paddle8 later collapsed separately.

The case exposes several errors that can arise in art-platform investment: treating transaction volume as equivalent to cash revenue, underestimating the cost of acquiring consignments, failing to protect client money and assuming that digital reach is a substitute for trust.

In conventional e-commerce, customers may tolerate a disappointing transaction and return later. In art, failure to pay a consignor or mishandling a valuable work can permanently impair the platform’s reputation.

The broader lesson is that rapid digital growth does not reduce the need for conservative working-capital management. It increases it, because seller proceeds may pass through the platform before the company has generated sufficient operating cash.

6. Winston Artory Group: combining judgement with infrastructure

The merger of Winston Art Group and Artory joined two assets that are often separated in the art market: human appraisal expertise and structured digital information.

The combination has a credible institutional buyer proposition. Family offices, insurers, trustees and lenders need independent valuations, but they also need a continuously updated record of ownership, location, condition and supporting documents.

The business is therefore positioned not merely as an adviser but as an administrative layer around collections. This should create greater revenue visibility than one-off appraisal assignments alone, although the extent of recurring revenue has not been publicly disclosed.

The transaction suggests that the next generation of art-technology deals will be less concerned with replacing experts and more focused on codifying their work.

7. Masterworks: financialisation without full liquidity

Masterworks raised $110 million in 2021 at a reported valuation above $1 billion. Its significance lies in turning interests in individual artworks into securities that can be distributed to a wider investor base.

The model creates an institutional acquisition platform and introduces asset-management economics into the art market. It can also generate data on investor demand and potentially expand the pool of capital available to selected artists.

However, the securities remain linked to an inherently illiquid asset. SEC disclosures warn of uncertain exit timing, potential losses, fees and risks relating to authenticity, physical damage and changes in artist popularity.

Masterworks should therefore be seen as a form of product and ownership innovation, not proof that the art market has become liquid.

Buyer universe: who is acquiring art-market businesses, and why?

Strategic buyers

Auction houses, logistics companies, marketplaces and professional-services platforms acquire businesses to obtain clients, specialists, geographic reach, data or adjacent capabilities. Their strongest advantage is the ability to realise revenue synergies: a regional auction house can direct major works into an international sale; a logistics provider can cross-sell storage; and an appraisal business can sell collection software.

Private equity

Private equity is most suited to art businesses with repeatable revenue, professional management and identifiable bolt-on targets. Bonhams is the clearest example.

The model is less convincing where EBITDA depends on a small number of consignments, artists or founders. Leverage can be particularly dangerous in cyclical businesses that may need to fund guarantees, inventory or extended seller-payment periods.

Family offices, wealthy individuals and sovereign investors

Patient private capital has long shaped the ownership of major auction houses. Christie’s is controlled through François Pinault’s Groupe Artémis; Phillips has been supported by owners associated with Mercury; and Sotheby’s is controlled by Patrick Drahi with ADQ as a significant minority investor.

Such buyers may value cultural access, international relationships, prestige and strategic positioning alongside financial return. Their investment horizons can also be longer than those of conventional funds.

Luxury groups

Luxury groups possess relevant customers, brand-management expertise and global distribution. They could theoretically acquire auction, collectibles or cultural-content platforms. Yet they must manage conflicts carefully: collectors may not want an independent auction house or adviser to become visibly subordinated to a commercial luxury brand.

The more likely opportunities are in adjacent categories such as watches, jewellery, design, fashion archives, collectibles and luxury resale.

Banks and wealth managers

Banks are natural participants in art advisory, lending and estate planning, but generally prefer capital-light services and collateralised credit to owning dealers or auction houses.

Acquisitions are most plausible in art advisory, valuation technology, collection reporting and specialist lending. Regulatory capital, conflicts and reputational risk make direct ownership of inventory-heavy art businesses less attractive.

Insurers

Insurers and brokers value risk data, condition records, valuation services and access to collector relationships. Partnerships may remain more common than acquisitions, but specialist appraisal, collection-management and risk-analytics businesses could become strategic targets.

Technology and venture investors

Technology investors initially concentrated on marketplaces, online auctions and NFTs. The more durable investment thesis is shifting towards professional software, data and trust infrastructure.

This reflects a broader realisation: the high end of the art market is not primarily constrained by the absence of an app. It is constrained by fragmented information, uncertain title, complex administration and the need for expert confidence.

Valuation and deal-structuring issues

Revenue quality

Buyers should separate recurring revenue from event-driven commissions, inventory gains and exceptional collections. Storage and software subscriptions usually deserve higher valuation multiples than one-off auction or advisory revenue because they offer greater visibility.

Inventory risk

Dealer and marketplace balance sheets require work-by-work diligence. Historic cost may bear little relationship to current value. Inventory may be subject to guarantees, artist restrictions, authenticity questions or informal profit-sharing arrangements.

Consignor and client concentration

A company may appear diversified while depending economically on a handful of collectors, estates or introducers. Buyers should analyse revenue by ultimate relationship owner, not merely by legal customer.

Founder and specialist dependency

Personal goodwill is one of the art market’s largest valuation risks. A buyer must assess whether relationships are institutionalised through teams, systems and contracts or remain attached to individuals.

Retention packages, deferred consideration, rollover equity and restrictive covenants may be required, but financial incentives cannot guarantee cultural loyalty.

Brand value

Art brands can be highly valuable but difficult to separate from reputation. Brand valuation should consider the durability of specialist expertise, consignor trust, artist relationships and the company’s ability to attract new clients rather than relying on historical prestige alone.

Working capital and client money

Auction and marketplace businesses may collect buyer funds before remitting sellers, creating potentially misleading cash balances. Diligence must examine segregation of client money, payment timing, guarantees, advances and aged consignor liabilities.

Cyclicality

Normalised EBITDA should be assessed across several market cycles. A peak-year multiple applied to peak-year earnings can overstate value dramatically.

Compliance and provenance risk

In the UK, qualifying art-market participants and freeport operators are subject to anti-money-laundering supervision for transactions at or above the applicable threshold. HMRC guidance has historically referred to €10,000, with internal guidance updated in 2026 to reflect a £10,000 threshold. Art-market participants also became subject to specified UK financial-sanctions reporting requirements from May 2025.

The US Treasury has identified sectors of the high-value art market as potentially presenting money-laundering and terrorist-financing risks, although its 2022 study did not recommend making the entire art market an immediate priority for comprehensive federal AML regulation. FATF has separately highlighted the exploitation of privacy, intermediaries and cultural objects by criminals and terrorist groups.

Buyers must therefore diligence customer identification, beneficial ownership, sanctions exposure, provenance, cultural-property restrictions, title, export licences and suspicious-activity procedures. Historic weaknesses can create contingent liabilities disproportionate to the target’s earnings.

Earn-outs, rollover equity and minority stakes

Earn-outs can bridge disagreements about sustainable earnings but are especially contentious in volatile art businesses. The seller may argue that weak results reflect market conditions or the buyer’s integration decisions rather than the underlying franchise.

Rollover equity can preserve alignment where founders and specialists remain important, although minority protections, information rights and leaver provisions require careful negotiation.

Minority investment may be preferable where the investor wants strategic access without disrupting culture or relationships. The ADQ investment in Sotheby’s illustrates how new capital can support deleveraging and growth while leaving control with the existing owner.

Why consolidation is difficult

The first barrier is cultural. Many art businesses define themselves through independence, connoisseurship and personal trust. Corporate ownership can be perceived as compromising judgement or placing financial return ahead of artists and scholarship.

The second is commercial. Key relationships are often non-contractual, inventory is difficult to value and revenue can be concentrated in a few unpredictable transactions.

The third is financial. Working-capital requirements can be substantial, particularly where businesses hold inventory, extend advances or provide auction guarantees. Cash conversion may differ materially from reported profitability.

The fourth is regulatory. Acquirers inherit exposure to AML, sanctions, provenance, title and cultural-property issues that may date back many years.

The fifth is integration risk. Centralisation may create cost savings but weaken the local identity and specialist autonomy that attracted clients. In art-market M&A, synergy extraction can destroy the asset if pursued too aggressively.

Outlook: the next five years

High-confidence trends

Infrastructure will consolidate faster than galleries. Logistics, storage, vertical software, data, collection administration and selected appraisal businesses offer more visible synergies and more transferable enterprise value.

Auction houses will continue to integrate vertically. Private sales, lending, luxury categories, estate services, data and digital tools can reduce reliance on public-auction commissions and deepen collector relationships.

Compliance capability will become part of valuation. Businesses with reliable ownership records, source-of-funds controls and provenance systems should be more attractive than competitors relying on informal processes.

Succession will generate opportunities—but not always conventional sales. Founder-led galleries and advisers will increasingly require transitions, but outcomes may involve management buy-outs, team transfers, partnerships or selective asset sales rather than straightforward acquisitions.

Data will become more valuable when combined with expert services. Standalone databases are useful; databases integrated into valuation, insurance, lending or collection-management workflows are more defensible.

Plausible but less certain developments

More sovereign and family capital may enter the sector. Cultural influence, luxury connectivity and long-term investment horizons make art infrastructure attractive, but the number of global trophy assets is limited.

Private credit may expand art-backed lending. The opportunity is credible, particularly for larger collections, but only where lenders can establish robust title, valuation, custody and enforcement procedures.

Artificial intelligence may trigger acquisitions of specialist technology. Image recognition, catalogue automation, anomaly detection and valuation support are likely targets. Fully automated authentication or valuation remains speculative because underlying evidence and expert accountability remain indispensable.

Gallery platforms may emerge around administration rather than artistic control. A shared-services model covering finance, logistics, compliance and technology could create scale while leaving artistic programmes independent. Whether galleries will accept such structures remains uncertain.

Fractional ownership may consolidate. Regulatory and customer-acquisition costs favour scale, but the viability of the sector will depend on realised—not merely reported or appraised—investor returns.

Conclusion

The art market is not becoming a conventional corporate sector. Its highest-value transactions will continue to depend on scarcity, judgement, discretion and trust.

But the commercial architecture surrounding those transactions is changing. Capital is moving towards businesses that can organise information, manage collections, provide liquidity, control logistics and reduce risk. That is where scale advantages are emerging and where the most credible M&A opportunities lie.

“The art world will not be consolidated by treating art like an ordinary product,” Baade concludes. “It will be institutionalised by building stronger businesses around the characteristics that make art extraordinary: its scarcity, uncertain value, complex ownership history and dependence on human judgement.”

The strategic winners will therefore not necessarily be the businesses that own the most art or employ the most recognisable specialists. They will be the platforms that can make an opaque market more efficient while preserving the confidence on which its value ultimately rests.

About the author

Dr. Daniel Baade is CEO of Dyer Baade & Company, an international M&A advisory firm, and previously served as Global Head of Strategy at Christie's, one of the world's leading auction houses. Combining senior leadership experience within the global art market with decades of advising founders, investors and private capital on complex transactions, he regularly advises on acquisitions, disposals, strategic partnerships, capital raising and succession across the wider art ecosystem.

About Dyer Baade & Company

Dyer Baade & Company advises founders, shareholders, family offices, auction houses, galleries, art-tech businesses and investors on strategic transactions across the global art market. The firm combines deep sector expertise with international M&A execution experience to help clients maximise value, identify the right strategic partners and successfully execute acquisitions, disposals, capital raising and succession transactions.

If you are considering selling an art-market business, exploring strategic acquisitions, raising capital or assessing long-term succession options, we would be pleased to discuss your situation in complete confidence.To arrange a confidential discussion with Dr. Daniel Baade, please get in touch.